Competition for new fintech customers is fierce. Particularly for the 1.4 billion people globally, who comprise the unbanked population, as estimated by the World Bank. Enter alternative data scoring — validating borrower credibility using data sources other than credit scores or rental payment data.

Alternative credit scoring allows lenders to validate the financial discipline of potential borrowers based on their digital footprints. Even without credit score data, lenders can engage these unbanked customers, thus increasing the bottom line in the face of the upcoming economic downturn.

From our experience, alternative data scoring ranks among 2023’s top fintech trends, and pairing it with a rigorous payment gateway integration process proved critical in projects like Molo Finance, the UK’s number one digital mortgage broker, and Money Park, the largest digital mortgage lender in Switzerland.

What is Alternative Credit Scoring?

Modern people leave digital footprints ranging from mobile data usage to utility bills, social media interactions, and mobile app payments. For example, utility bills paid on time go under the radar for credit bureaus, while they show financial discipline and are an important factor in alternative credit scoring.

All of these alternative credit data sources allow businesses to create precise digital profiles of customers — including customers with low credit scores from traditional credit rating bureaus, such as immigrants, students, young people just joining the workforce, first-time homebuyers, and rural farmers.

Credit scoring using alternative data enables lenders to validate applicants and serves the unbanked population by letting them start building successful credit profiles.

Implementing custom fintech software solutions with alternative credit scoring requires aggregating data from multiple sources, in various formats, normalizing it, and processing it with AI algorithms. This isn’t easy, but the benefits of using alternative data sources for credit scoring outweigh the challenges of implementation. This is how.

Industry

Empower your finance services digitalization.<br />

Alternative credit scoring fintech solutions are reshaping the way lenders assess creditworthiness. Traditional ones involves processing data from past banking, credit card, and loan transactions. Alternative credit scoring fintech bureaus like TransUnion, Experian, and Equifax record and analyze the credit history of US and/or EU citizens and provide this data to lenders for moderate fees. Needless to say, first-time borrowers like students, recent graduates, and many immigrants who don’t have thick credit files often struggle to get their first loan approved — especially when decisions rely solely on traditional data sources instead of alternative credit data.

While homeownership and having substantial sums in the bank are excellent loan feasibility indicators, quite a large portion of the population does not meet those criteria, even if they are perfectly able to repay loans.

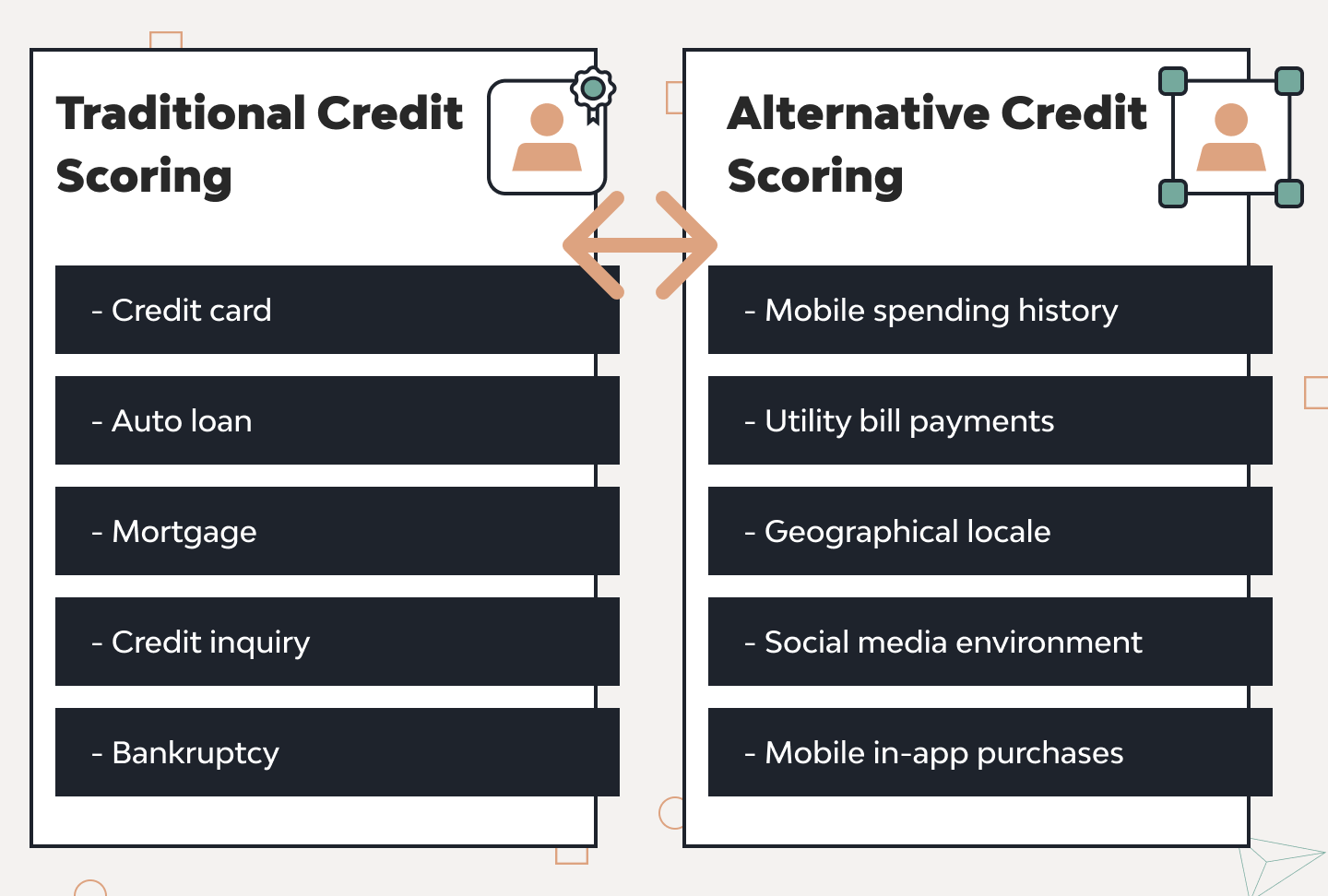

This calls for using alternative credit scoring models, which evaluate people based on a multitude of additional parameters, including, but not limited to:

Mobile spending history

Utility bill payments

Geographical locale

Social media environment

Mobile in-app purchases

What’s more, using this alternative credit data for grants better visibility into the status of borrowers with short credit histories, making it possible to offer them better rates than they would get from competitors and still make a profit.

How Does Alternative Credit Scoring Work, And What Data Does It Use?

Lending has three core aspects: stability, ability, and willingness.

Applicants should be able to show they are financially stable enough to repay the loan and should prove they are able and willing to make regular repayments. When patterns from their previous credit history are available, validating these core aspects is easy. But when there aren’t any bank accounts or previous loans, alternative credit data can help fill the gap through alternative data scoring.

Paying for a mobile carrier, short-term rental properties like Airbnb or online subscriptions like Spotify and Netflix, and regularly paying utility bills are all positive spending habits. They can show that customers who might be first-time borrowers in a given country are actually financially stable and responsible enough to repay a loan.

For instance, many Millennials and Zoomers actively avoided using credit cards and taking long-term loans after the financial crisis of 2008. Thus, they don’t — and maybe never will — have long credit histories, even though they may actually earn and spend a lot. How can lenders assess their financial situation, then? Through digital footprints that contribute to an alternative credit score.

Lenders can use the phone number or email provided on loan applications to look up customers’ social media profiles on Meta, Twitter, Telegram, Snapchat and their accounts on other platforms like Airbnb, LinkedIn, Pinterest, Microsoft 365, and Discord.

If such profiles exist, the alternative credit score data provider can also use API calls to gather other details like lists of contacts and payment history. This data contributes to (or detracts from) the customer’s credibility and sufficiently replaces a traditional consumer credit history for verification and validation purposes.

All of this also helps verify that the borrower is a real person, not a fraudster with throwaway credentials.

Digital footprints left across multiple data points can provide an accurate representation of a customer’s spending patterns. When traditional records are missing, scoring with alternative credit data enables onboarding of no-hit applicants long overlooked by mainstream banks. Alternative credit scoring fintech solutions make this possible by leveraging non-traditional data to assess creditworthiness more inclusively.

However, for alternative credit scoring fintech companies, handling diverse sources isn’t trivial. Solutions need pipelines to ingest unstructured, multi-format batches; normalize for analysis; and demand significant investment across analytics, risk, model training, and AI integration.

Types of Alternative Credit Data Used by Lenders

Lenders today increasingly turn to alternative credit data to evaluate borrowers who lack traditional credit history. These non-standard indicators offer a fuller, data-driven view of financial behavior and risk potential.

Spending Patterns and Financial Behavior

Tracking how users spend, save, and manage recurring payments helps assess financial discipline. This goes far beyond checking income—it reveals true financial habits over time.

Alternative Loan Repayment Histories

Performance on microloans or peer-to-peer platforms reflects borrower reliability, even without formal credit records. It offers crucial insight into repayment consistency.

Bank Account Balances and Assets

Consistent balances, savings activity, and asset growth serve as strong stability indicators, particularly for thin-file borrowers or those with irregular income.

Income Verification and Employment Documents

Verified pay slips, freelance contracts, and income streams build a clearer picture of repayment ability. Lenders use this alternative credit data to assess stability.

Credit and Debit Transaction Data

Spending categories, payment timing, and cash flow patterns help lenders assess risk based on real behavior, not assumptions—an essential part of alternative credit data models.

Social Media and Online Behavioral Data

Used carefully, digital behavior supports identity verification and fraud prevention, adding one more layer to modern alternative credit data ecosystems.

How to Collect Alternative Credit Data

There are two main approaches to collecting alternative credit data:

Through custom-built solutions developed by an IT service provider

By integrating with an existing data provider like Experian via an API

DjangoStars has used both approaches. While integrating a ready solution via fintech API is quicker and cheaper at first, it can become costly in the long run — especially for an alternative credit scoring fintech product. We’ll explain why later.

But some alternative credit scoring fintech products are not built to integrate with data aggregator platforms like Experian. In such cases, the only option is to develop a custom alternative credit scoring solution using artificial intelligence to gather and process unstructured data.

Naturally, there are privacy and fraud concerns, as most customer data contains personally identifiable information (PII). Thus, alternative credit scoring solutions must be built in compliance with data privacy and security regulations around the world, like GDPR, the CCPA, PSD2, open banking, and certain FTC regulations.

Alternative Credit Scoring Models

Manually reviewing massive amounts of alternative credit data in all its various formats is, of course, impossible. This is where AI algorithms and ML models become indispensable for powering alternative credit scoring models. After properly training an algorithm of AI in finance, it can quickly scan vast arrays of publicly available data and identify patterns, even in unstructured data.

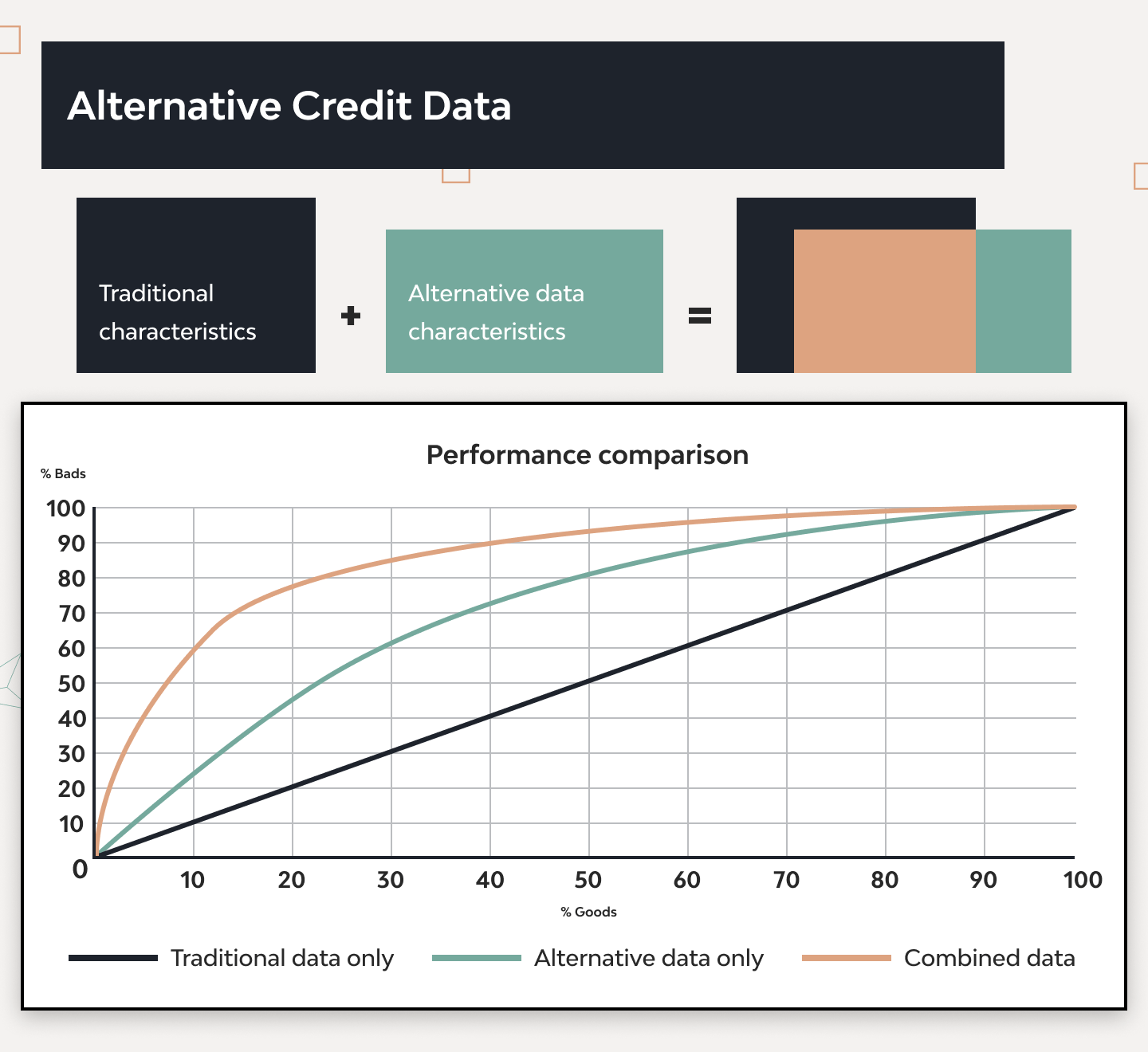

As FICO’s research states, combining traditional and alternative data sources for lending helps create a more in-depth understanding of an applicant’s financial discipline. They enriched conventional banking data with details like these:

Fine details of transactional data

Telecom/utility/rental data

Social media profiles (although they assigned little value to it because it raises privacy concerns and can be manipulated)

Social network analysis (identifying a customer’s different social accounts and connections with people)

Behavioral analysis of the interaction with websites

Text and audio data (from credit applications and previously recorded customer service conversations)

Survey data (see below for how we used survey input in our projects)

Although a risk model developed by FICO demonstrated the high value of traditional credit reports, nearly 60% of its predictive power also came from nontraditional sources. FICO emphasized that incorporating alternative credit scoring models led to much more accurate predictions, despite some overlap in the insights provided by both types of information.

Most importantly, the alternative data makes it possible to validate the creditworthiness of credit-invisible individuals and clients with thin or no credit files.

AI and ML for data processing

AI algorithms and ML models enable lenders to comb through all the traditional consumer credit files and enrich the dataset with real-time insights from social media interactions, mobile payments, online purchase histories, and more than five hundred other parameters to gain additional data points. API integrations play a vital role in this process by accessing storehouses of available customer data from credit bureaus and other data providers.

Naturally, alternative credit scoring models are cloud-based systems, so their building blocks include features from AWS, Google Cloud, Microsoft Azure, or other cloud platforms, along with third-party services from data aggregators.

Benefits of Alternative Credit Scoring for Borrowers and Lenders

The biggest advantage of alternative credit scoring fintech solutions is their ability to tap into the pool of credit-invisible customers. This population presents an opportunity for lenders to greatly expand their customer base, which is especially important in the face of the upcoming recession. It also benefits first-time borrowers by solving the problem of having a thin credit file.

In addition, alternative credit scoring in fintech looks at real-time data about customer payment patterns, which supplements consumer credit scores. Large credit bureaus hold some data for up to ten years (which might be outdated), while alternative data sources access real-time information gathered from recent rent payments, subscriptions, telecom data, eCommerce spending, mobile purchases, and bookings of rental properties and flights.

Other benefits of alternative credit scoring fintech solutions include the ability to offer better interest rates to your competitors’ existing clientele and dramatically faster, more cost-effective underwriting using AI, which leads to an improved customer experience. Let’s look at these points in more detail.

More accurate creditworthiness assessment

People tend to change payment patterns with time. They might lose a job and miss a couple of payments or get a better job and repay a loan early. They might win the lottery and start spending big or deposit this money to use as capital to start a business, then apply for a loan to grow quicker. Due to all sorts of changes in life circumstances, a person’s creditworthiness might rise or decline over time.

Assessing a customer’s credit at the exact moment they apply for a loan is very important for accurate risk profiling, as it uses real-time information from sources and about events not included in traditional reports. With alternative data and credit scoring, lenders can assess risk with up-to-date details and form a real-time, more holistic picture of their customer’s credit profiles.

This also helps fight fraud — incorporating over five hundred data parameters helps lenders identify malicious actors much faster than they can with only a traditional credit history.

Improved customer experience

Automated alternative credit scoring models use machine learning to significantly cut the time and cost of loan origination and reduce the number of inevitable errors humans make during underwriting. This allows lenders to offer lower rates, making their offers more competitive. As a result, they create a positive customer experience for both new and existing clients.

For example, based on a customer’s current payment history and spending habits, a lender can convince competitors’ clients to transfer their loans for a better rate — this results in market share gains and improves the company’s bottom line.

Increased market reach

Reaching those 1.4 billion people who are under- and unbanked presents an enormous opportunity. While these people might have meager credit profiles, their online payment habits and alternative credit data might show them to be creditworthy customers for lenders willing to issue loans to first-time borrowers.

Using alternative data for credit scoring opens additional income streams by serving underbanked population segments who had little chance of being approved for loans through traditional credit scoring data.

Real-World Examples of Successful Alternative Credit Scoring Implementation

A recent report from the Hong Kong Monetary Authority shows alternative credit scoring usage growing at a steady pace across the US, Europe, and Asia. Alternative credit examples are community development financial institutions (CDFIs), the EU-based CRIF (Credit Information and Finances), and the US-based Small Business Financial Exchange (SBFE). Let’s delve deeper into each.

CDFIs

Community development financial institutions are lenders across the US and the UK. They serve smaller customers who fall outside the scope of traditional banks, and the majority of their loans range from $30K to $100K. CDFIs have in-depth knowledge of particular market segments and can determine the creditworthiness of businesses with thin credit files.

Technological advances enable CDFIs to increase their outreach and underwriting speed, so they can now also act as third-party data providers for loan assessments. DjangoStars used this approach when building Molo Finance and Money Park platforms.

We designed APIs that integrate with third-party services like CDFIs. This way, when a customer wants to check if they are qualified for a mortgage, they use our tool to request data from a third-party service. This online service enriches the data submitted by Molo Finance or MoneyPark customers with information gathered from alternative data sources to tell the borrower whether they qualify for a mortgage or not.

It’s always worth noting such API requests are paid for, which means:

It’s better to use mock data instead of real integration because wealth management software development might cost a fortune otherwise since you would be paying a third-party service for test API calls.

This feature should be available only to registered borrowers. With Molo Finance and Money Park, we prevented unwarranted expenses by preceding a mortgage calculator with an in-depth input form requesting specific financial data needed for mortgage origination. This way, only registered customers actually interested in receiving a mortgage use this feature.

Integration with third-party data aggregators like Experian and other services is a great way to validate customer credibility with high accuracy, even if they have thin or none credit files.

CRIF

Founded in 1988, CRIF is an EU-based global provider of financial data solutions and one of the leading alternative credit scoring companies, supporting lenders and businesses across five continents. After CRIF successfully implemented PSD2 compliance (a set of EU electronic payment regulations) as a part of their open banking initiative, they were able to engage new market segments using alternative credit scoring methods.

CRIF helped an Italian multi-regional banking group implement alternative data sources for lending. This meant the bank could now evaluate a person’s and business’s creditworthiness using a combination of financial data and other data sources. The bank gained richer customer insights, leading to improved up-selling and cross-selling of specialized banking products.

As a result, 22% of the bank’s customers adopted new banking products, which were marketed based on information the bank learned about companies’ seasonal activity and international import/export records. In addition, 19% of the bank’s customers conducted business with firms that had good credit histories. These firms were outside of the bank’s client base, providing opportunities for the bank to recruit new customers.

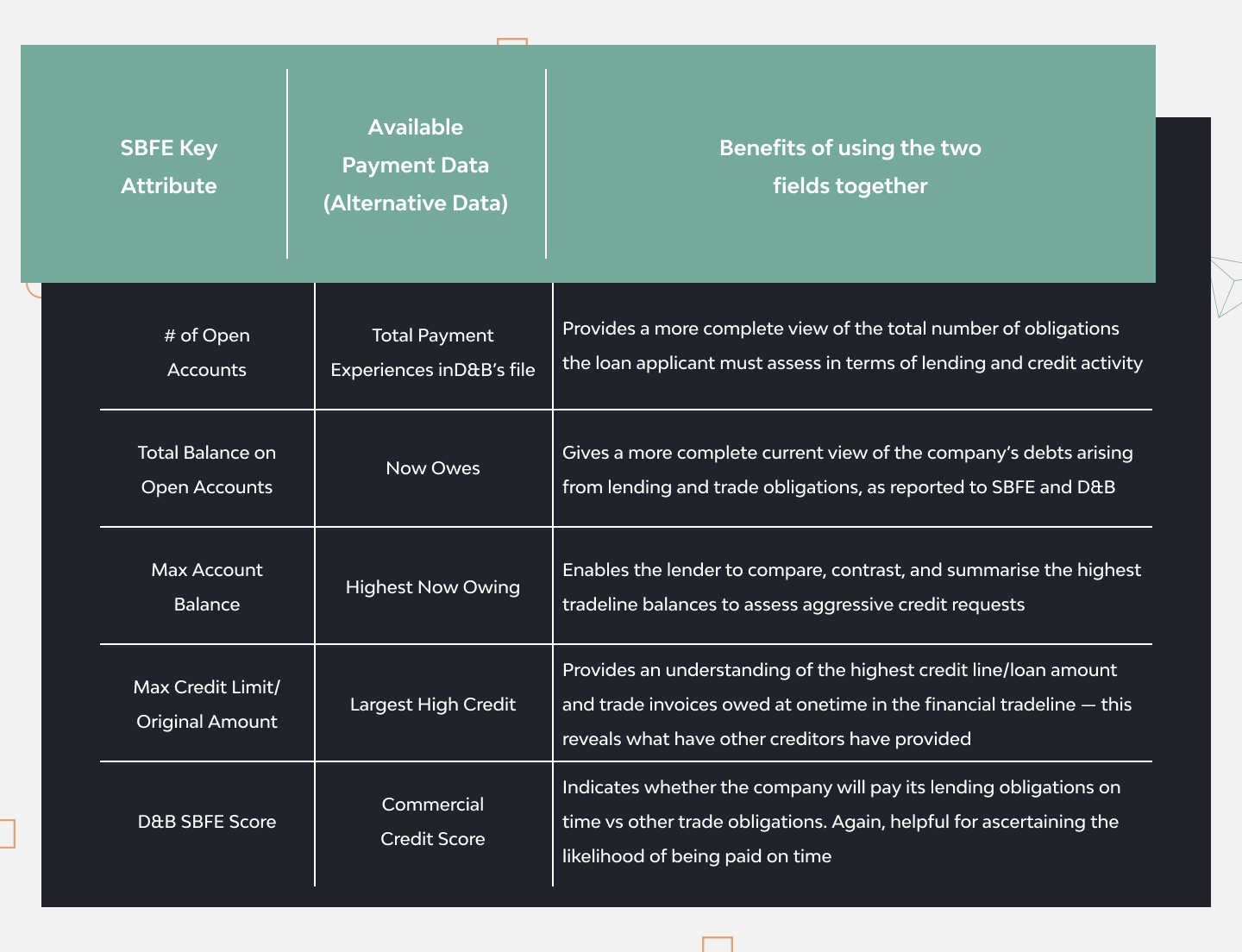

SBFE

The Small Business Financial Exchange is a highly-trusted financial body founded in the US in 2001 and governed by the small business lending industry. It operates independently of the big three credit bureaus (Experian, Equifax, and TransUnion).

SBFE provides credit reports to small lenders that accurately assess the financial health of business loan applicants using a combination of SBFE’s internal and external data. The external data comes from vendors certified by SBFE, such as Dun & Bradstreet. For example, here is what combining the data looks like when Dun & Bradstreet assesses a loan applicant.

Alternative data sources for scoring help lenders worldwide build accurate risk models at scale and quickly assess applicants’ financial reliability at a relatively low cost. This creates vast opportunities and signals a strong future for alternative credit scoring fintech firms focused on delivering innovative lending services.

The Future of Alternative Credit Scoring

Alternative credit scoring is on the rise, providing a means for lenders to reach under- and unbanked populations. It will prove especially vital in view of the upcoming recession, where attracting new customers and retaining existing clientele are crucial, not only to survive the economic downturn but to emerge stronger.

By combining traditional and alternative credit data, lenders can more accurately assess risk and make informed loan decisions based on customers’ real-time spending habits and discipline. This benefits both B2B and B2C segments, opening new revenue streams for fintech businesses and providing access to financing for customers without traditional credit scores.

Implementing alternative credit scoring features also provides a strong competitive advantage. Fintech companies using alternative credit data sources will be able to differentiate themselves from conventional lenders by serving unbanked populations.

However, alternative credit scoring implementation might not be feasible for every fintech company. It requires significant investments in risk assessment, artificial intelligence, and machine learning. Therefore, deciding to implement alternative data sources for lending should be informed by an in-depth analysis of your company’s current and future strategy, the market landscape, customer expectations, and your resources.

Should you plan to implement alternative credit scoring for your product, contact us for an in-depth consultation on this topic based on your particular situation. We at DjangoStars stand ready to lend our rich fintech development expertise to help achieve your goals!

Thank you for your message.

We’ll contact you shortly.

Frequently Asked Questions

What are the challenges and risks of alternative credit scoring?

Data ownership and fraud are the two biggest concerns, followed by discriminative lending. Alternative data gathering should comply with GDPR and other regulations. Data should be stored securely to prevent misuse by fraudsters, and scoring should not be biased or lead to discriminative, preferential lending.

Are there any regulatory challenges for alternative credit scoring?

Yes — a lot of alternative data sources are tightly regulated by the GDPR, PSD2, the CCPA Act, and open banking and FTC regulations. In addition, access to these sources requires secure data practices to protect PII. However, all of these can be handled by an experienced software development partner.

How accurate is alternative credit scoring compared to traditional credit scoring?

Alternative credit scoring is based on accurate real-time data on the spending habits and financial discipline of a person or company. While these have lesser weight than traditional credit scores, it helps validate applicants with thin credit files or those with none at all. This is essential to increase the borrower audience and attract new customers.

How does using alternative credit scoring improve the lending process?

Automation with ML models helps significantly shorten loan origination and underwriting, decrease costs, and prevent human errors. It also allows lenders to offer better interest rates to the clientele of their competition, which benefits all parties included.

Post Views:13,966

Table of content

Want to start a project ?

Hire experienced developers to build your next project with DjangoStars

We store cookies on your computer. We use these cookies to collect information about how you

interact with our website and remember you. We use this information to improve and customize your

browsing experience and for analytics and metrics about our visitors both on this website and other

media. To find out more about the cookies we use, check our Privacy Policy.

Subscribe

to our

newsletter

Thanks for

joining us! 💚

We’ll let you know, when we got something for you.