At DjangoStars, we follow best practices for insurance software development and emphasize the importance of thoughtful planning in custom insurance software development. We recommend businesses focus on the following when building an insurtech management platform.

subscribe

Fintech Technology & Dev Insights for Startups & Enterprises

Fintech Tips & Strategies for Building Financial Solutions

Insurance Software Development: The Ultimate Guide to Insurtech

Updated: Aug 15, 2025

/

22 min

read

Artur Bachynskyi

CEO

After a slow start, insurtech is finally catching up with regtech, proptech, and other parts of the larger fintech industry. Both global consortiums and local market players are starting to build software for insurance, invest in ready-made solutions, or partner with insurtech startups. What’s more, things look set to accelerate: the insurtech market was valued at $7.87 billion in 2022, with revenue forecast to be $152 billion by 2030, growing at a CAGR of 52% year-on-year.

The rise in insurance software development investment makes sense since industry players need to be agile and adapt to survive the economic downturn. A 2022 KPMG survey reveals that 77% of insurance CEOs have a digital transformation strategy in place to ensure they remain competitive.

“Driving transformation and increasing efficiency by utilising technology across the front, middle and back office will likely be crucial for insurers as they develop operational ambitions for the next three years.”

– Mark Longworth,

Global Head of Insurance Advisory KPMG International

Therefore, for insurance companies of all sizes, the question is not so much whether to digitalize with insurtech but how to do it.

There are three viable approaches:

- Buy a white-label software solution

- Partner with an insurtech startup

- Make a custom insurance software platform, either internally or through a technology vendor like DjangoStars

Throughout our work in insurance software design and development, we’ve seen the benefits and disadvantages of each option. The first one — buying a white-label solution — is a no-brainer.

The second one, partnering with an insurtech startup, can help established companies reduce expenses by automating underwriting and time-consuming backend processes. Still, there are many things to consider:

- Whether the insurtech startup has a proven record of successful collaboration with insurance companies

- Whether the company can provide sufficient levels of cybersecurity for the product

- Whether the startup has good standing with investors and will be able to deliver on their product development promises

- Whether the cost of their services is prone to change when the product scales up in terms of infrastructure and API request numbers

The third approach — developing insurtech software solutions from scratch — brings its own considerations. We will showcase them in this article to help companies make informed choices.

Types of Insurance Software

As a starting point for insurtech software development, let’s explore the types of ready-made and custom insurance software solutions a company might need to offer. Naturally, some tools are more useful than others in different niches (P&C, health insurance, auto insurance, pet insurance, etc.).

- User claim processing software. These solutions automate insurance claim management, submissions, and collections. They usually include a customer relations management system (CRM) and an accounting module, among other features.

- Insurance document management software. This integrates different communication channels into a central dashboard to efficiently capture and process claims, case files, and other documents. The result is improved data processing, policy management, regulatory compliance, pre-qualification, and more.

- Insurance underwriting and rating software. Digitizing underwriting activities frees up company time and resources while delivering reliable results. Risk management software for insurers aids in identifying, assessing, and mitigating risks in underwriting and policy management, promoting a strategic approach to risk coverage and pricing.

- Agency management software, inclusive of CRM functionalities. It streamlines agency operations by managing client data, policy administration, commission tracking, and ensuring all interactions and customer correspondence are centralized for operational efficiency and enhanced service quality.

- Insurance portals and customer-facing apps. These provide digital gateways to policy information, claims submission, and account management through web and mobile platforms. They play a vital role in digital customer engagement strategies, offering transparency and convenience for all parties involved.

- Policy administration software. This facilitates the management of the entire lifecycle of an insurance policy. Features often include policy issuance, endorsements, renewals, and cancellations, enhancing efficiency in policy operations.

- Fraud detection software for insurance. Utilizing advanced analytics and machine learning, this software helps in identifying potentially fraudulent activities within insurance claims. It can analyze patterns and anomalies in claim submissions, reducing the risk of financial loss due to fraud.

- Insurance billing and payment software. This software streamlines the billing cycle with automated invoice generation and payment processing, supporting varied payment methods to boost customer satisfaction and financial management.

- Regulatory compliance management software. With the ever-changing insurance regulatory landscape, this software helps companies stay compliant with local and international laws. It can track changes in legislation, manage compliance documentation, and ensure that all processes are in line with regulatory requirements.

- Quoting software. It streamlines the quoting process with automated risk assessments, delivering personalized and accurate quotes rapidly to potential customers.

- ERP (Enterprise Resource Planning) for insurance. This integrates core business processes in financials, HR, and operations specifically tailored for the insurance sector.

- Data analytics and BI (Business Intelligence) software. This leverages complex data sets to enhance decision-making across all areas, including risk assessment, trend forecasting, and claims processing efficiency. It supports informed strategic decisions, optimizing pricing models, and improving customer service.

Alongside the type of insurtech platform they adopt, companies need to plan for the future. Survivors in the market are the companies that can adapt fast to trends in insurtech.

Must-Have Features for Insurance Software

In insurance software development, different companies require different tools to operate efficiently — but most custom insurance software solutions share several core features. These include:

- Claims activity monitoring

- Mapping and mitigating risk parameters

- Tracking of processes

- Risk analysis and calculation

- Payments processing

Claims activity monitoring

Whether it offers time-tested reactive claim management or more technology-savvy preventive claims monitoring, an insurance platform must support claims activity monitoring. This allows companies to pinpoint the root cause of the issues to minimize losses, prevent fraud, and ensure an optimal customer experience.

Mapping and mitigating risk parameters

Insurable risks also vary from customer to customer. Mapping and mitigating these risks can improve both insurer profits and customer well-being.

As an example, data from the insurance company The Hartford shows that 75% of all water damage claims originate from accidental discharge of HVAC systems, appliances, and plumbing. Advising customers to install water leakage sensors is a simple step that can help save property and reduce the number of insurance claims.

Risk analysis and calculation

Risk analysis of natural or manmade disasters plays a key role in determining insurance policy rates. The accuracy of risk analysis increases as more regional and historical claims data is taken into account. For example, flood damage claims are common in the southeastern part of the USA, while fire damage claims are more prevalent in Western regions, where droughts are regular.

This is why having a risk calculator powered by AI algorithms and big data analytics is crucial for calculating risk possibilities and offering competitive policy rates.

Process tracking

Customer-centric insurance companies need to stay on top of every task in progress, from underwriting to policy adjustment and handling ongoing cases. The decision to build your own custom insurance software can ensure transparency and visibility with a dashboard that showcases all the processes and their stages.

Payments processing

An integrated payments processing module is essential for centralizing financial operations and cash flow. Incoming and outgoing payments can pass through a wide range of gateways and payment service providers. This means insurance automation software must be capable of interacting with them via secure API integrations.

Any competitive insurtech solution will have these five core features. Depending on the project, a platform may also include other features such as reporting and analytics or a separate mobile app.

Insurance Software Development Process

Insurance software development, especially when building an app from scratch, is a complex process that demands extensive technical and marketing expertise — yet, in most cases, the development and adoption steps follow a similar pattern.

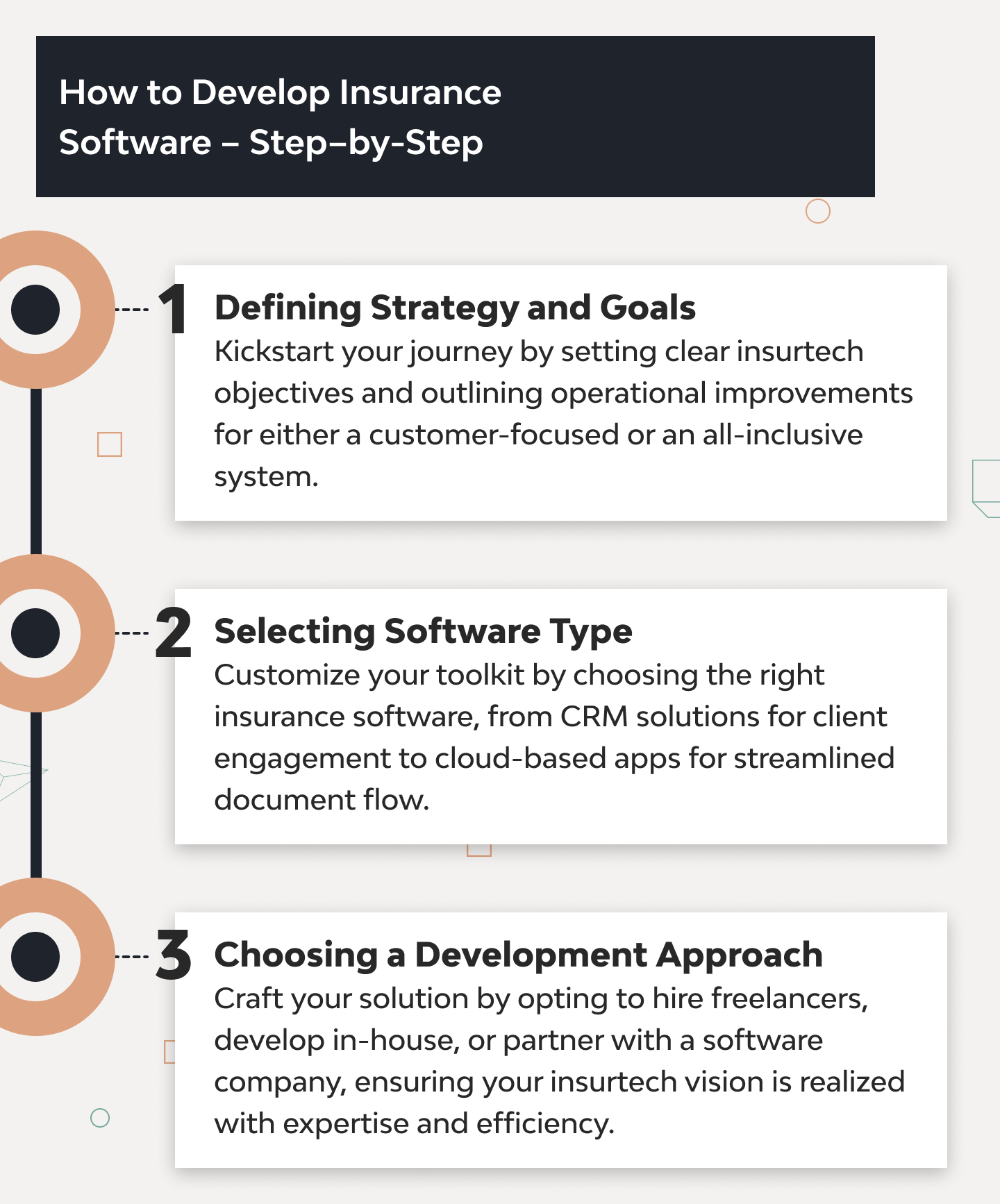

Here are the three steps to design a convenient and profitable insurance app.

1. Define your insurtech strategy and business goals

Before creating insurance software, the first and foremost thing is defining what operations and processes you need to improve or simplify by an app. It may be a point solution for customer services only or a full-fledged all-in-one system that allows one to arrange any insurance and pay for it in minutes.

Based on the implemented business model, an app must meet the company’s tech and non-tech requirements.

At the beginning, specify all activities you need to improve. They may be general business goals like reducing operational costs and increasing customer loyalty or concrete objectives like creating a solid online system allowing customers to perform all insurance-related actions only by smartphone.

The more detailed the goals are, the more accessible developers can design what you need.

2. Choose the insurtech software type

There are various types of insurance software. Each solves a specific task or a problem, so choose carefully.

For example, if you want to boost lead management processes and improve communication with clients, CRM-based insurance software is the best choice. And if you want to simplify the document flow and speed up the insurance application process for customers, an app based on a cloud solution is preferred.

Still, there’s no need to pick a single solution. When designing custom solutions, most insurance companies combine multiple features from different software types.

3. Pick the development approach

Maybe it’s the most crucial decision because the entire development and integration process depends on it. Here are the options:

| Hire a freelance development team | It’s the cheapest solution but not the safest one. You will face significant risks, such as various communication issues and low quality of the created software product. |

|---|---|

| Build the insurance solution in-house | It may be the best way if your development team has required tech expertise. Recall that engineers must deal with AI and ML, APIs and microservices, blockchain, and about a dozen other technologies. Moreover, insurance software development requires deep knowledge of Python, R, Scala, MatLab, Java, and other programming languages and frameworks. Only a few teams in the entire market have such tech stacks. |

| Hire an experienced software development company | It’s the best choice in terms of quality and terms. And that’s why:

|

If you want to make the development of insurtech software smooth and easy, contact us.

Which Technologies Are Used in Insurtech?

Like most innovative industries, insurtech is built on new technologies. We expect the next phase of insurance software projects to be tightly connected to artificial intelligence, big data analysis, and blockchain. Indeed, the emphasis in the insurance industry is shifting from core services to AI-powered analytics and a more personalized customer experience. Thus, having AI and big data features is no longer an option but a necessity.

1. Artificial intelligence and machine learning

Insurtech solutions use AI and ML for internal process optimization and automation, which cuts the cost of routine work and streamlines mundane tasks. Machine learning is particularly useful for automating claims settlement: by eliminating the human factor, AI makes claim processing faster, cheaper, and more accurate.

2. Big data analysis

Data is key to improving relationships between companies and users. Today, it’s not enough to know who uses a product — companies also need to understand how, when, and where it’s being used. This is where big data, integrated into custom insurance software, plays a transformative role.

Big data delivers valuable insights for insurance companies aiming to stay ahead of the curve. It enables better risk assessment and underwriting, reveals market trends, and powers AI- and RPA-driven operations. When built into custom insurance software, these capabilities translate into more accurate pricing, faster service, and a customer experience that’s truly data-driven — especially when combined with inputs from sensors and IoT devices.

3. APIs and microservices

Integrating third-party solutions helps insurance companies offer innovative services faster. As we’ve already said, those who miss the moment to digitize will eventually fall behind.

APIs, pre-built libraries, and microservices all help integrate existing solutions into a product. This saves time and money compared to developing app features from scratch. For instance, a third party might provide a feature that checks customer data to prevent fraud and abuse.

4. Blockchain

Blockchain is a revolution for insurtech. Its role in strengthening security, preventing fraud, and building effective reinsurance systems has made it one of the major technologies used in insurtech solutions today.

The very nature of smart contracts makes the blockchain system almost impossible to break or defraud. For example, the blockchain’s shared immutable ledger and the ability to analyze large numbers of data points make it easier to detect fraudulent claims.

By leveraging cutting-edge technologies, companies are not only enhancing operational efficiency but also significantly improving service quality.

Challenges in Insurance Software Development

While digital transformation is reshaping the insurance industry, building scalable solutions isn’t without obstacles. Here are the key challenges companies face in insurance software development:

Legacy Systems Integration

Integrating new tools with legacy systems can create data silos, slow performance, and raise compatibility issues. Modernization is a major hurdle in insurance software development.

Data Security and Compliance

Handling sensitive personal data means full compliance with regulations. Insurtech software development must prioritize encryption, secure access, and data governance.

Regulatory Requirements

Laws vary by country and product type, so staying compliant during development and scaling is complex. Insurtech software solutions must be built with adaptability to changing legal frameworks.

Scalability and Flexibility

Solutions must evolve with the business — whether it’s handling more users, new markets, or additional services. Lack of flexibility in architecture can stall growth and increase technical debt.

Cost and Time Management

Developing high-quality insurance products on time and within budget is a balancing act. Poor planning or unclear requirements can lead to overruns, missed deadlines, and rising costs.

Current Trends in Insurance Software Development

Whether the decision is to build an insurtech platform from scratch or simply add insurance management features to an existing solution, one thing is important: developing insurance software doesn’t just equal putting insurance forms online.

In fact, all good insurtech software development has to incorporate current market developments and trends, such as:

- A focus on digital consumers. Insurtech is geared towards customer satisfaction, not operational efficiency alone, and products need to be targeted at a new digital-savvy generation.

- Cybersecurity. Data leaks and breaches can spell doom for an insurance company, which makes security a key priority.

- Outsourcing and using existing solutions and tech stacks. As insurtech gains pace, time-saving strategies like these help minimize time-to-market when developing new software or updating legacy solutions.

Let’s delve deeper into each point.

A focus on digital consumers

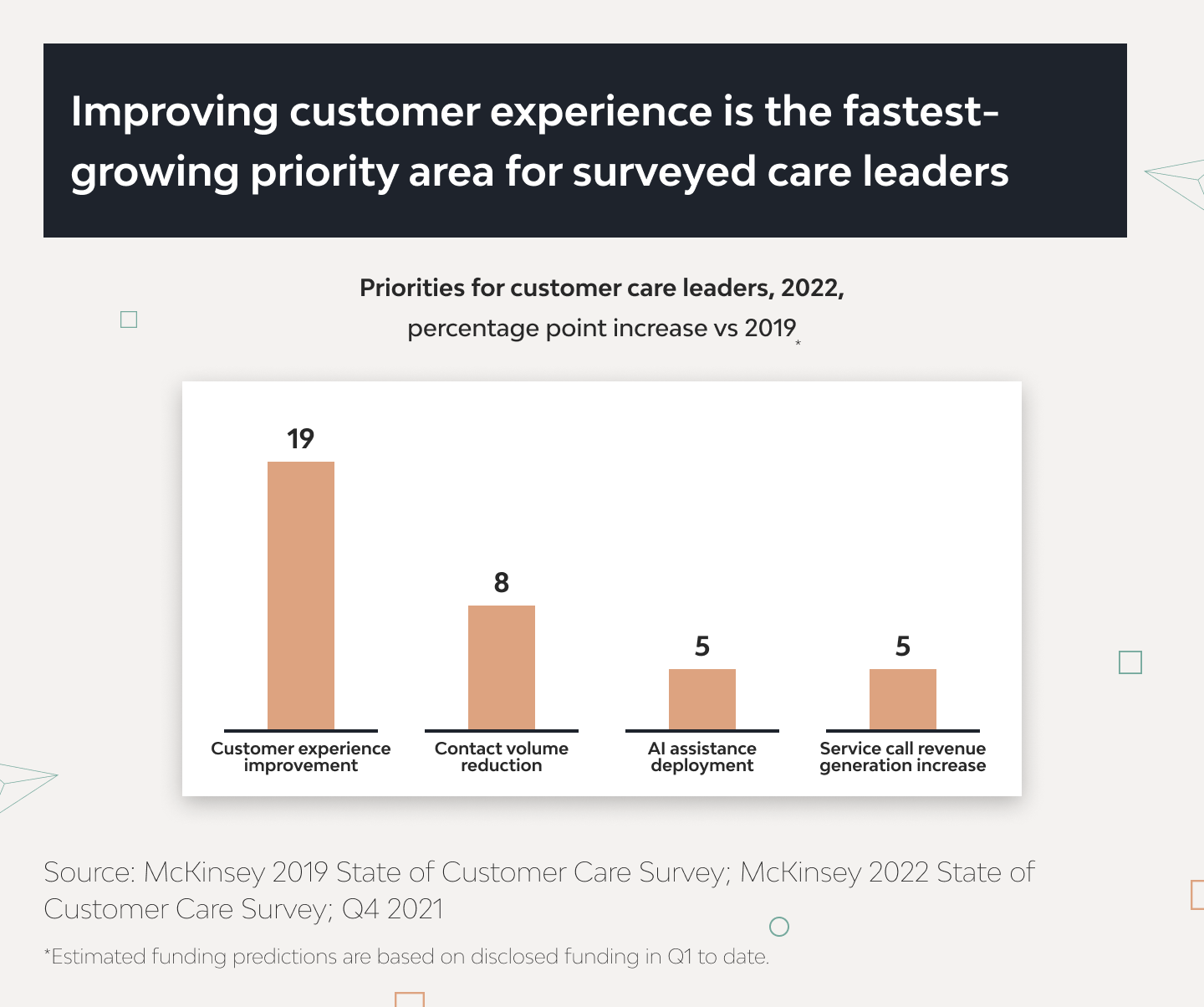

McKinsey’s 2022 survey on the state of customer care highlights customer experience as key to surviving the recession.

This means that customers need to be placed squarely at the center of a product concept before fintech software development services even begin. What pain do they need to solve, what will the communication process be, and how will a solution ensure data security, streamline payments, and provide a transparent audit trail?

Just as important is looking at customer engagement: how a company will connect with a prospect to turn them into an interested lead and then a paying customer. Door-to-door marketing and cold phone calls are becoming less effective in the digital era. Millennials and GenZ may be constantly interacting with their phones, but it’s easy to block and blacklist a number. New times bring new customers who require new offerings.

Millennials are unlikely to go to an insurance office to insure something they purchased online or something that doesn’t fall into a standard insurance category. Instead, they might want to insure a device borrowed for a weekend or a VR set just delivered from Amazon. As a result, solutions need to support multiple communication channels and automated self-service features such as chatbots, automated quoting, and payout approximation tools.

Cybersecurity

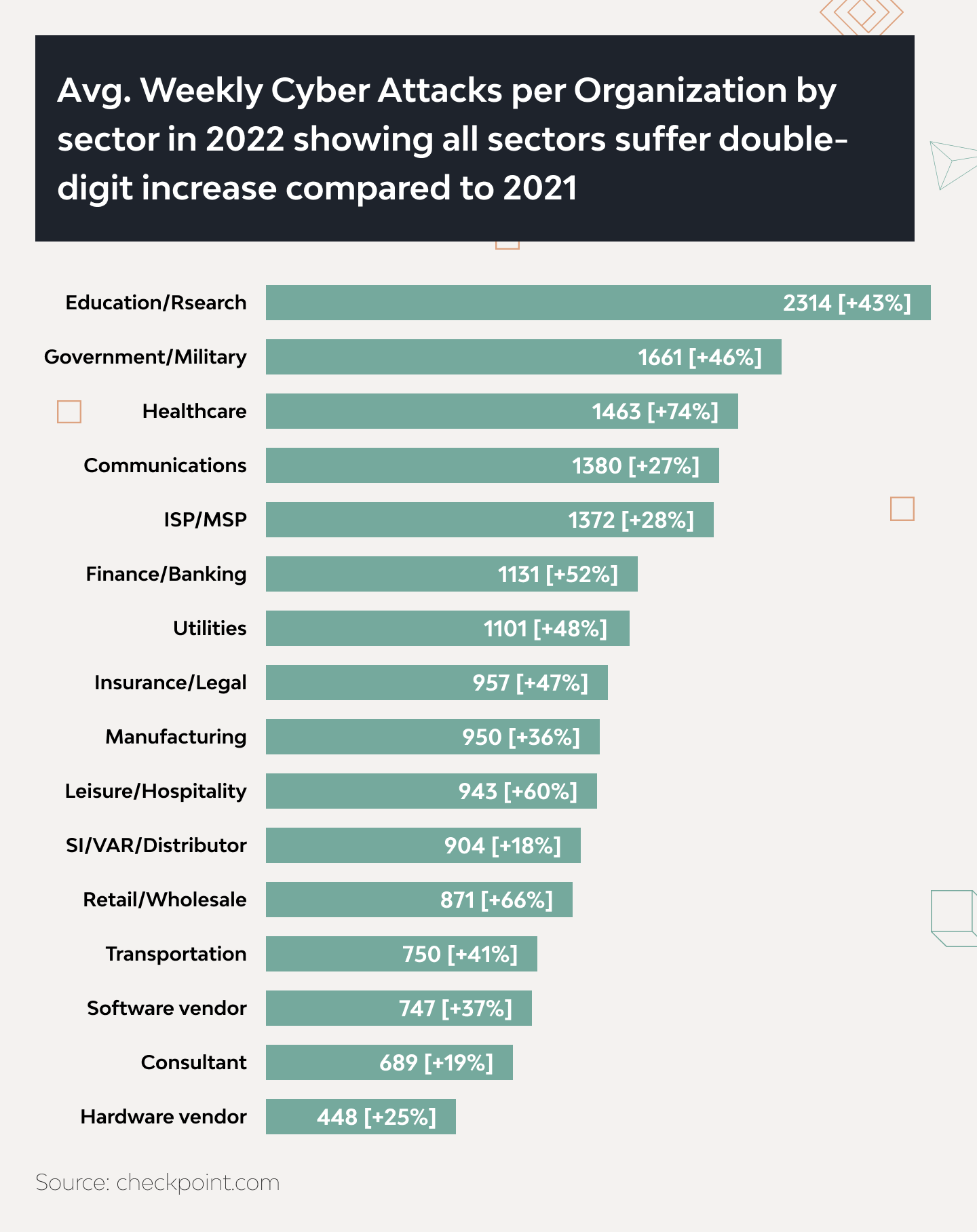

Data breaches and personal data leakage are on the rise. While the insurance industry is not the most prominent target, it faced a 47% increase in cyberattacks from 2021 to 2022. This places it above the average 38% increase in cyberattacks across all sectors.

Yet in an Ernst & Young survey, 75% of insurance business owners did not feel it was “very likely” that they would be able to detect a sophisticated cybersecurity attack. Clearly, the majority of insurtech players feel endangered by cybersecurity threats.

To address this challenge during product design and development in insurance, it’s best to be strategic and proactive rather than defensive and reactive. With the majority of cybersecurity breaches originating from outside organizations, the strongest cybersecurity strategies combine big data analysis with blockchain-based and AI tools to detect and head off attacks.

Outsourcing and using existing solutions and tech stacks

While both security and customer experience count, ensuring minimal time-to-market is also important. Companies need to choose the most viable and time-efficient approach and minimize risks. This could mean buying an off-the-shelf solution, developing from scratch in-house, or outsourcing to an insurtech development agency.

The main questions when choosing between a ready-made solution or developing a new product/feature are: what is the core value this software should deliver, and what customer needs should it satisfy?

With the answers in mind, it may be possible to find an acceptable off-the-shelf product at a reasonable price.

If no solution is available, these two answers will drive the development approach. They will also dictate the resources needed for development and ongoing support.

In DjangoStars’ experience, the win-win situation for companies who need more than a ready-made solution is to build custom insurance software with an outsourced team. This has several benefits:

- An insurance company can overcome internal capacity and legacy code constraints.

- An experienced outsourcing partner can provide ready solutions for some development challenges, thus shortening the product delivery cycle.

- An outsourced team will know the best api integrations for fintech, libraries, and modules for different use cases. This makes development more efficient without compromising the quality of deliverables.

We’ve briefly mentioned popular technologies such as blockchain, AI, big data analytics, and APIs that can be used when developing digital insurance software. Let’s take a closer look at the value they can provide.

Best Practices in Insurtech Development

Sandbox testing

A sandbox testing environment lets developers deploy new software modules and run tests against anonymized data sets to check system performance under different conditions. With a separate testing environment, companies can ideate, iterate, and rapidly test new ideas without endangering mission-critical data and processes. This way, customers and operational data stay secure.

Scalability from the start

Nobody wants to discover that the insurance platform they built can’t scale. Successful projects begin with a clear framework that outlines the initial features, the individual stakeholder responsibilities, the metrics that determine success, and the decision-making criteria. With this framework in place, an insurance automation system scales alongside the business and continues to drive value instead of becoming a bottleneck.

DjangoStars always considers scaling at the start of a project and plans the product architecture accordingly. This way, scaling a product up or down is easy, as there’s no need to refactor code or significantly modify the product when it needs change.

APIs and integration play a crucial role in scalability, so let’s talk about this aspect.

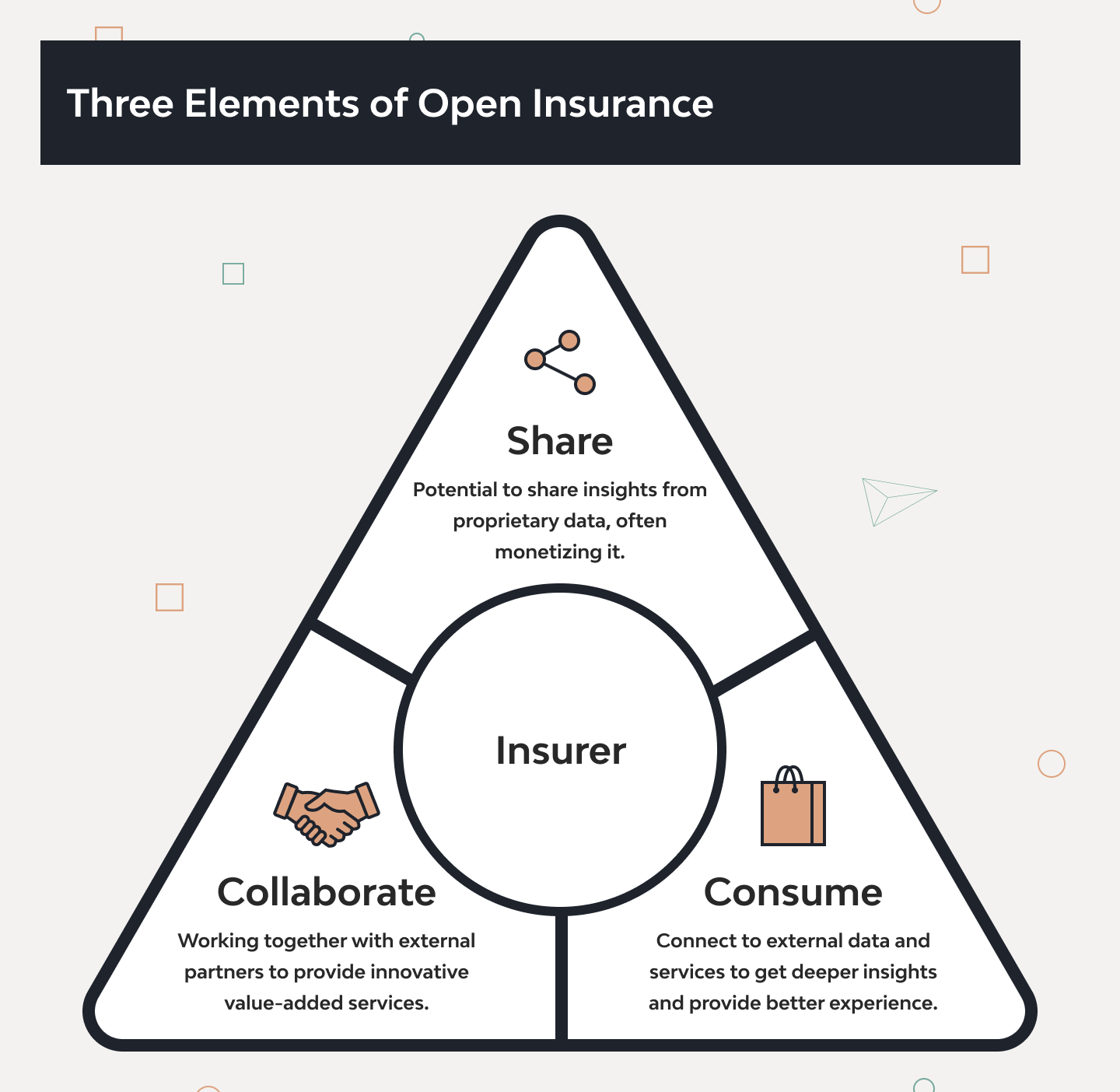

Third-party service integration

Just as the banking sector uses open banking, modern insurance processing has its own open insurance model. Instead of siloing data and paying for storage, insurance providers can get data from third-party service providers via APIs.

Open insurance gives insurers valuable agility in a volatile market. For example, while property and casualty insurance has long been a sector staple, the 2022 World of Insurance report from Capgemini highlights a shift to consumer concerns about climate change and resilience. Many insurers have had to integrate additional data sources to meet the new demand (53% of surveyed added up to 6 new data sources to their decision-making process). Open APIs make such adjustments possible and therefore keep companies more competitive.

Real-Life Insurance Software Solutions

Let’s examine real-world use cases that demonstrate the effective use of these features in insurtech. These examples highlight how insurance software projects succeed not only in their technical execution but also in delivering tangible benefits—enhancing service delivery and boosting customer satisfaction across the industry.

1. Lemonade: Automating Insurance Processes for Swift Claim Settlements

Lemonade is a relatively well-established startup that focuses on protecting property and homes, and it’s often highlighted as a benchmark for successful insurance software projects. They are famous for their significantly low prices, which they manage to achieve by automating a huge part of their internal workflow. For example, most claims are handled by a chatbot that can render decisions in seconds if the case is easy or otherwise pass the case to a claims team.

Lemonade’s workflows have reduced the time needed for claim settlement to one day on average, compared to an average of 11 days for manual settlement before automation.

2. TrackActive: Harnessing Data Analytics for Enhanced Rehabilitation Outcomes

TrackActive offers patients and their doctors a better and more efficient path to rehabilitation after injury. Using the app, a doctor can prescribe exercises, monitor patient activity, and help patients recover faster.

TrackActive’s behavioral app receives data from a patient’s smartphone or smartwatch, which tracks their physical activity, heart rate, and blood pressure. Analysis of this data gives the doctor insights into recovery progress, along with possible risks and what can be done to prevent them.

3. MoneyPark: Seamlessly Integrating Insurance Services

MoneyPark, a platform we’ve been working on since 2012, provides personalized advice on insurance and mortgage products in Switzerland. Its main feature is a convenient and fast search for the best mortgage offers on the market. However, when the customer gets a mortgage, the platform offers insurance for the mortgage as an option.

Though the major part of the product was developed from scratch, calculation operations for insurance are driven by a third-party library from a Swiss firm Logismata. In MoneyPark, insurance is both a separate service and an additional feature that helps increase customer satisfaction. It’s an example of how smoothly some features of an insurtech product can be developed or integrated by using an existing open-source or third-party library.

4. Arbol: Utilizing Blockchain for Climate-Based Risk Insurance

Arbol is a US-based fintech company that provides insurance against climate-based risk through advanced insurtech software solutions. Arbol uses Ethereum-based smart contracts to automate its backend execution and improve coverage efficiency. The company’s data- and blockchain-based workflows eliminate the need for manual settlement processes and dramatically accelerate claims processing and payments.

Building a successful product means choosing the right technologies, following insurance software development best practices, and building must-have features.

How to Ensure Insurtech Software Security

Integrations and the open insurance model help companies stay agile and respond to market shifts quickly, but they also introduce new security concerns. In insurtech software development, securing access to data—especially when working with third-party sources and services—is critical. Leveraging software microservices is one of the most effective ways to address this challenge.

When an application is made up of a group of modules, each running as a separate microservice within a Docker container maintained by a Kubernetes/Terraform cluster, this offers multiple layers of protection. Each container is secure by design and has built-in alerting and monitoring mechanisms, so if a fraudulent request is detected, the affected microservice can be shut down and rebooted on the fly without affecting overall platform performance.

In addition, the structures in a microservice environment provide granular access and security policies enabling in-depth monitoring of all activities. When configured correctly and backed up by other cybersecurity measures, these features can boost insurtech security.

How Much Does It Cost to Develop Insurance Software?

Many factors influence the cost of custom insurance software. On average, building a barebone MVP with minimal features takes around 200 working days — roughly 1,600 hours. With hourly rates in Eastern Europe ranging from $30 to $50, the starting cost typically falls between $48,000 and $80,000. This figure can vary depending on several variables, such as the feature set, the number of planned integrations, and the expected scalability.

If a product already exists, additional time is needed to analyze its structure and either integrate new features or rebuild parts from scratch. That said, experienced teams with a well-developed module library and refined processes can reduce development time significantly — bringing both costs and time-to-market down.

Final Word: Insurtech Is the Future of the Insurance Industry

A few years ago, insurtech felt more like hype than a source of real value. But with the rise of tech, AI, and blockchain, it’s clear the industry is gaining momentum — and insurance companies that don’t embrace custom insurance software development risk falling behind.

In summary, here are our four key pieces of advice to new insurtech developers:

- Develop for digital-savvy consumers. Operational effectiveness is no longer an effective KPI: everything now revolves around customer satisfaction. It’s imperative to gather customer data, analyze it, use the insights to build and improve the product, and then measure customer satisfaction.

- Don’t skimp on security. Personal data leakages are a major reputational problem and can kill a product in a moment.

- Stay focused. When creating a product that will hopefully win the market, it’s tempting to implement a long list of features. But in the words of MoneyPark CTO Benjamin Tacquet, “Sometimes you want to do too much. My best advice is to do less, but better.”

- Don’t delay. Digitization is rapidly transforming the insurance industry, and the longer a company postpones its digital transformation, the fewer chances it will have to regain a competitive advantage.

Of course, a strong and reliable development partner is also critical to success.

At DjangoStars, we have over nine years of expertise in building fintech and insurtech products, the question “what is regtech?” doesn’t kick us in the gut—we translate it into compliance-by-design architecture, KYC/KYB and AML pipelines, automated regulatory reporting, and audit-ready data trails. Our average partnership period is 2.5 years, and our core clients — national leaders in fintech and insurtech — stay with us for 6+ years. It’s a wealth of experience ready to be shared in our next insurtech project. Contact us, and let’s help modernize your insurance services with custom insurance software solutions!

Thank you for your message.

We’ll contact you shortly.

Frequently Asked Questions

- What makes insurtech revolutionary?

- First, insurtech automation helps reduce the time and costs associated with all insurance processes, which results in much more affordable insurance policy rates. Second, insurtech makes insurance much more attractive, accessible, and understandable for modern consumers. Third, it opens up opportunities to serve niches outside of traditional insurance categories, such as small businesses (Next Insurance), disabled persons or people with long-term health conditions, pet owners who want to travel (Many Pets), or those who want to drive a borrowed car (Cuvva).

- What are the benefits of insurance software solutions?

- The core benefit is offering insurance both as a standalone product and as an embedded experience with other financial services (like covering a mortgage). This creates a value-added network of companies, insurtech startups, and SaaS players who are all focused on delivering next-level customer experience to modern digital customers.

- How long does it take to create insurance software?

- The time required depends on the scope of the task, whether any existing code has to be incorporated, and the number of features to be included. As a rough figure, it takes around 200 working days to develop an insurtech MVP with standard core features.

- What are the challenges in insurance software development?

- The main challenges include:

- Correct product design and development in insurance to allow for future scaling.

- Secure access for third-party APIs to enable data exchange.

- Implementing big data analytics and AI/ML features.

- Is it worth creating a custom insurance solution, or is it better to use a ready-made one?

- As always, it comes down to business goals and budget. Many ready-made and economical solutions solve basic insurance automation challenges. However, they can lack important features and integrations or, conversely, charge for functionality that isn’t needed. In this case, custom insurance software development is a better option.

Want to start a project ?

Hire experienced developers to build your next project with DjangoStars

related article