Molo

The first fully digital mortgage provider in the UK.

From considering the target country and assembling an experienced team to choosing the right technology for future scalability, third-party integrations, and tools for communication. We’ll cover all key aspects that can set a fintech product on the path to success.

As the financial technology (fintech) industry continues to grow and evolve, more and more businesses are considering building their own fintech products. However, there are several important factors to consider before embarking on such a project.

Our team at DjangoStars, providing custom software development for fintech since 2008, comes across these considerations frequently in practice. The tips below reflect our developers’ extensive experience in the domain.

Financial technology, aka fintech, is a popular startup sector for entrepreneurs, as more and more people are striving for financial literacy. The shift to treating one’s finances more intelligently has led the creators to apply the principles of human-centered design (HCD) when developing fintech products.

However, knowing good design is not enough to start a successful fintech company. In this article, I will tell you all about the pitfalls that await almost anyone who has decided to build a new fintech product.

Fintech product development is exerting a revolutionary influence in today’s competitive market. It drives innovation, enhances customer experiences, and allows us to meet the evolving needs of the financial industry.

For users, a well-executed fintech product means efficient and convenient financial services, streamlined processes, and personalized solutions. For organizations, fintech product development is an opportunity to capitalize on emerging trends in the financial sector by leveraging technology, data analytics, and user-centric design.

Thus, if a company strives to stay ahead of the curve, attract and retain customers, and gain a competitive edge, it can hardly overestimate the importance of building a successful fintech product. After all, it is a way to achieve sustainable startup growth and long-term success in the dynamic fintech landscape.

Building a fintech product requires careful planning, strategic decision-making, and a deep understanding of the financial industry. And, of course, it is best to be accompanied by an experienced team on this journey. Let’s explore the essential steps to create a fintech product that stands out in the market and delivers value to its users.

Fintech aims to substitute for (or improve on) traditional financial institutions by delivering more efficient methods of engaging in financial activities. Governments regulate all financial bodies and services, except cryptocurrencies. This makes it difficult to introduce new approaches to providing financial services, whether they are investments, online banking, or any other sector, unless they are lawful.

So before starting a fintech company, study the regulations in your target country of operations. You cannot predict all the challenges along the way, but you can minimize losses by complying with the existing rules. Otherwise, you can become subject to fines or a ban from doing fintech business.

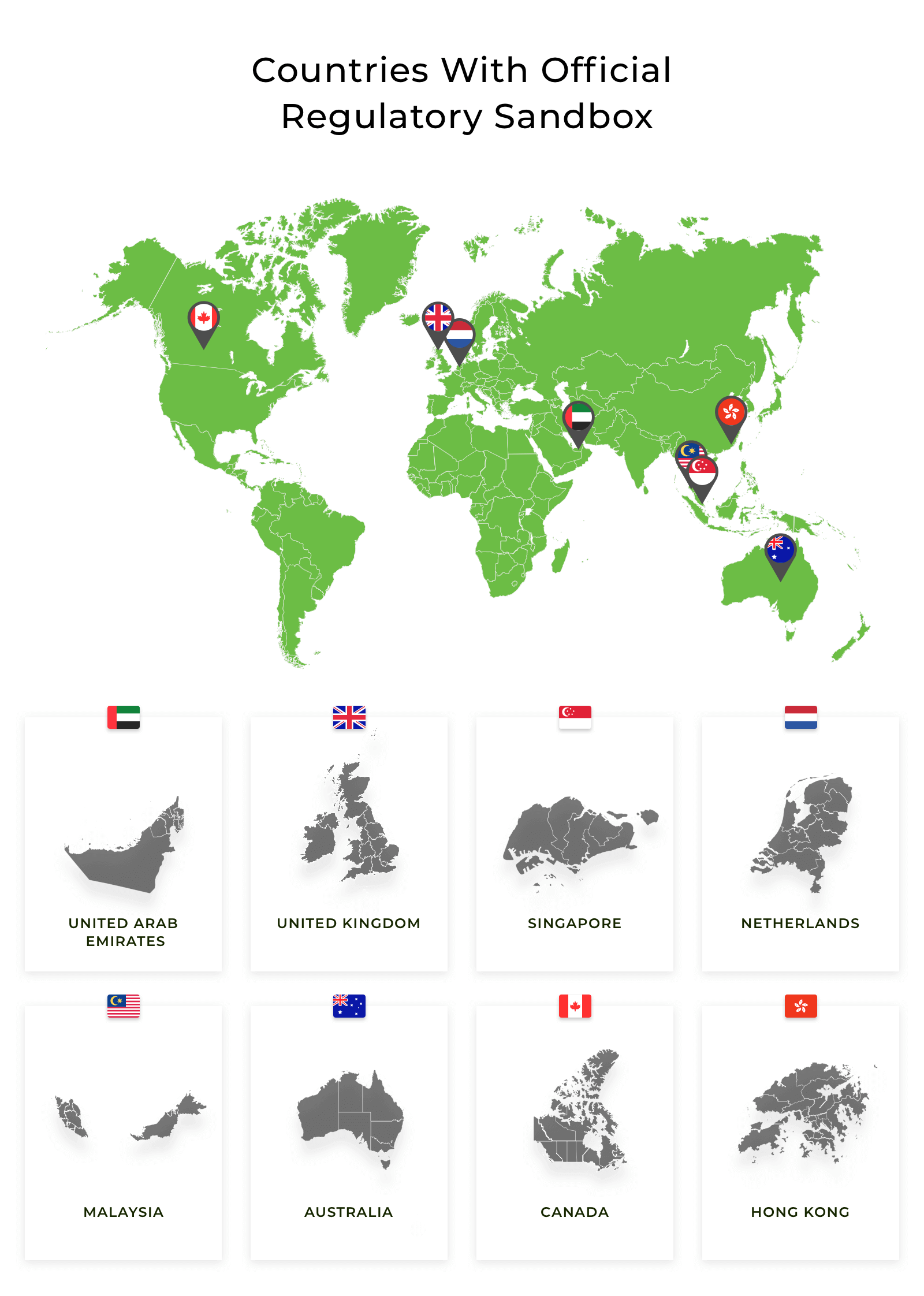

For example, eight countries in the world have launched a regulatory sandbox in their financial markets. This means that they have created a special framework, governed by the local financial center regulation, to enable the testing of innovative technologies under regulatory supervision.

It is not only fintech that must abide by strict, government-regulated policies. If you are doing healthcare business in the US, you also have to comply with the Health Insurance Portability and Accountability Act (HIPAA). Basically, it is a set of rules that every healthcare-related business has to follow, since they work with (or may have access to) protected patient health information. This is an obstacle for many healthcare startups that cannot afford multiple fines, ranging from $50k to $1m a year.

Make sure to study the financial sector you are going to enter, but better yet, hire a specialist. It would be a huge disappointment to learn that your startup is breaking the law right before its launch.

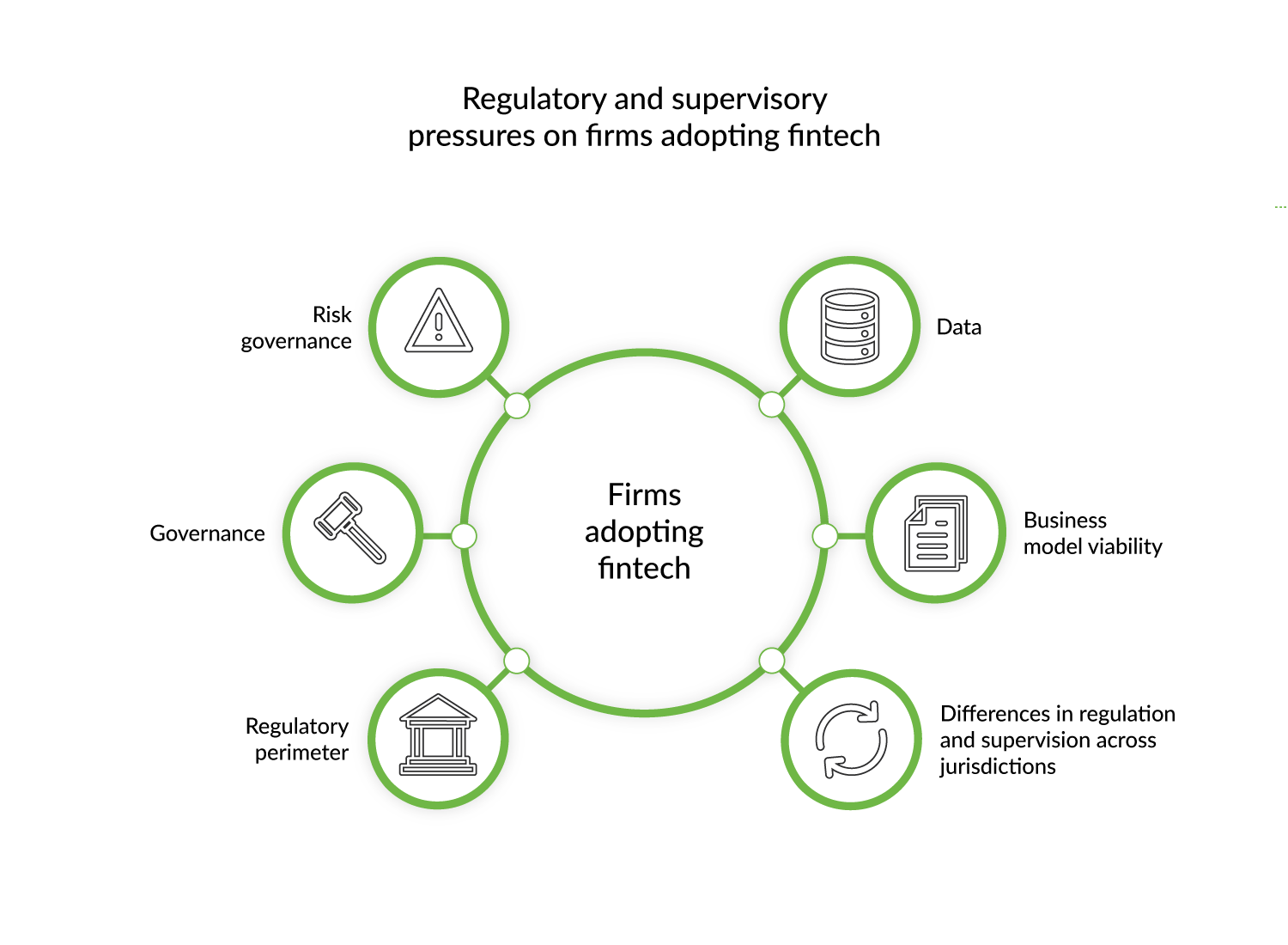

Without a doubt, fintech products provide a range of benefits both for investors and consumers. However, the rapid growth of fintech companies has also triggered different risks related to consumer protection, data privacy, and governance.

That’s why regulators and supervisors have developed standards and rules for everyone entering the fintech industry or starting a fintech startup. These rules change frequently, so make sure you continuously review them—make such checks an internal part of your business strategy, even.

Let’s look at what regulations a fintech startup can be subject to.

The Federal Trade Commission (FTC) is a bipartisan federal agency that protects customers from deceptive commercial practices. It conducts investigations, sues companies that violate the law, and collects complaints about data security and misleading advertising.

Recently, the FTC has paid much attention to the fintech industry. For example, it sued Lending Club in 2018, which provided loans to customers “with no hidden fees”. As it turned out, in reality, Lending Club was sneaking in (often behind obscure hyperlinks) charges of a 5% fee.

The key lesson from the FTC’s actions is that companies should always be truthful and transparent with their customers and avoid hidden fees.

This government agency makes sure that lenders, banks, and other financial institutions don’t deceive people.

Recently, the Consumer Financial Protection Bureau launched a US consumer network for fintech. This network will promote regulatory certainty for financial innovators and help companies stay tuned for changes in the fintech space.

Here are some things that every fintech business should know about GDPR:

Anti-money laundering laws are created to prevent illegal financial operations. The purpose of AML rules is to detect suspicious activity such as money laundering, terrorist financing, securities fraud, and market manipulation.

Fintech solutions can reinforce the AML efforts of banks with the help of blockchain technology and machine learning. It’s an opportunity to make it easier for banks to comply with AML rules.

These are only some of the best-known fintech regulations. Make sure you do your legal research, read the acts and rules before you push your product onto the market.

Before developing a fintech product, make sure it complies with recent fintech regulations. Here are some actions you should take:

Examine the legal norms of the country where the startup is going to work

For example, as we have already mentioned, some countries, such as Singapore, Australia, and the UK, have Regulatory Sandboxes.

The regulatory sandboxes are created by governments and banks as a space for fintech startups to conduct testing with temporarily adjusted regulations. Sandboxes help companies ensure that their fintech startups are secure and won’t become subject to any violations.

However, in the United States, fintech companies must comply with both federal and state laws.

Answer the following questions:

Reach out to the community and lawyers for advice

Reach out to a network of entrepreneurs who deal with the fintech niche. You can learn a lot from their experience and advice. It’s also recommended to have a financial lawyer specialized in securities law on your team who will analyze how different regulations can affect your business.

The popular slogan “to design good products, find experienced people” is the key to a successful release. Unlike many industries that software engineers deal with, fintech is stuffed with financial jargon—terms that non-financial people will not understand. Therefore, within the framework of fintech product development, it is extremely important to find people who have experience with it.

In each fintech startup, there is always someone from the finance world who can ensure that the team will not be confused by industry-specific terms, like APR and AER. If you do not know what these two acronyms stand for, I have made my point. When you build fintech engineering teams that are knowledgeable about a sector, say investments, you will avoid misunderstandings.

Plus, developing an online financial service gets easier with experience, gradually reducing the chances of an error occurring. So hiring savvy, experienced fintech software developers can:

It does not mean that each engineer has to have a degree in finance, but the tech lead or senior engineer should be acquainted with the subject matter.

Together with our clients, we build fast and easy-to-use digital solutions changing the mortgage industry.

Let’s build yours.

If you know an experienced team that has little or no knowledge of finance, you could teach them, say, by setting up recurring workshops or seminars. If the team does know a few things about finance, you should describe your vision of the domain and the problems your startup is going to try to tackle.

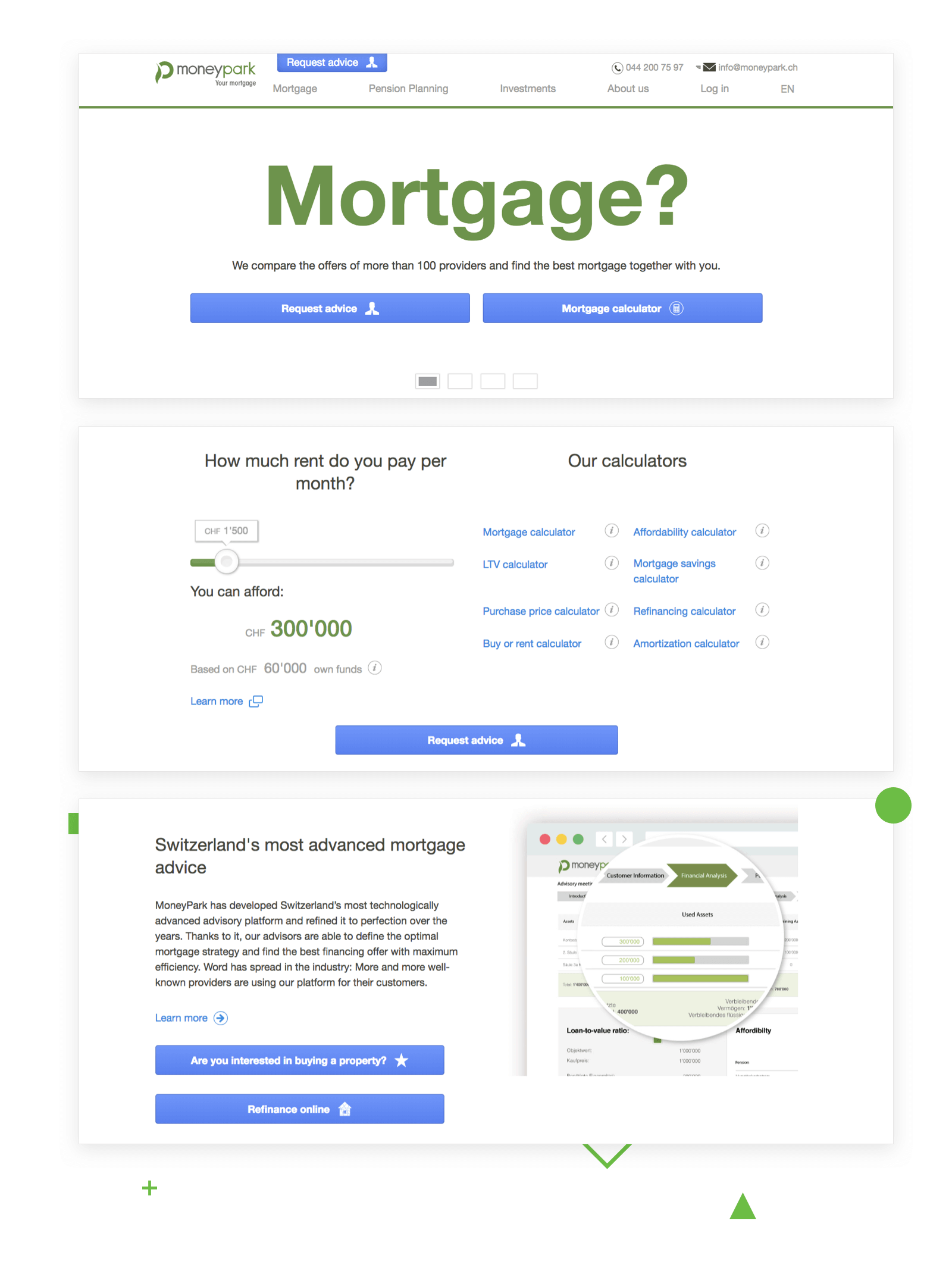

Just like when our Django development team was working on MoneyPark, a Swiss online mortgage service, our clients used to organize a workshop for our team so that they understood the terminology and felt confident with financial products. But I will return to MoneyPark later in the article.

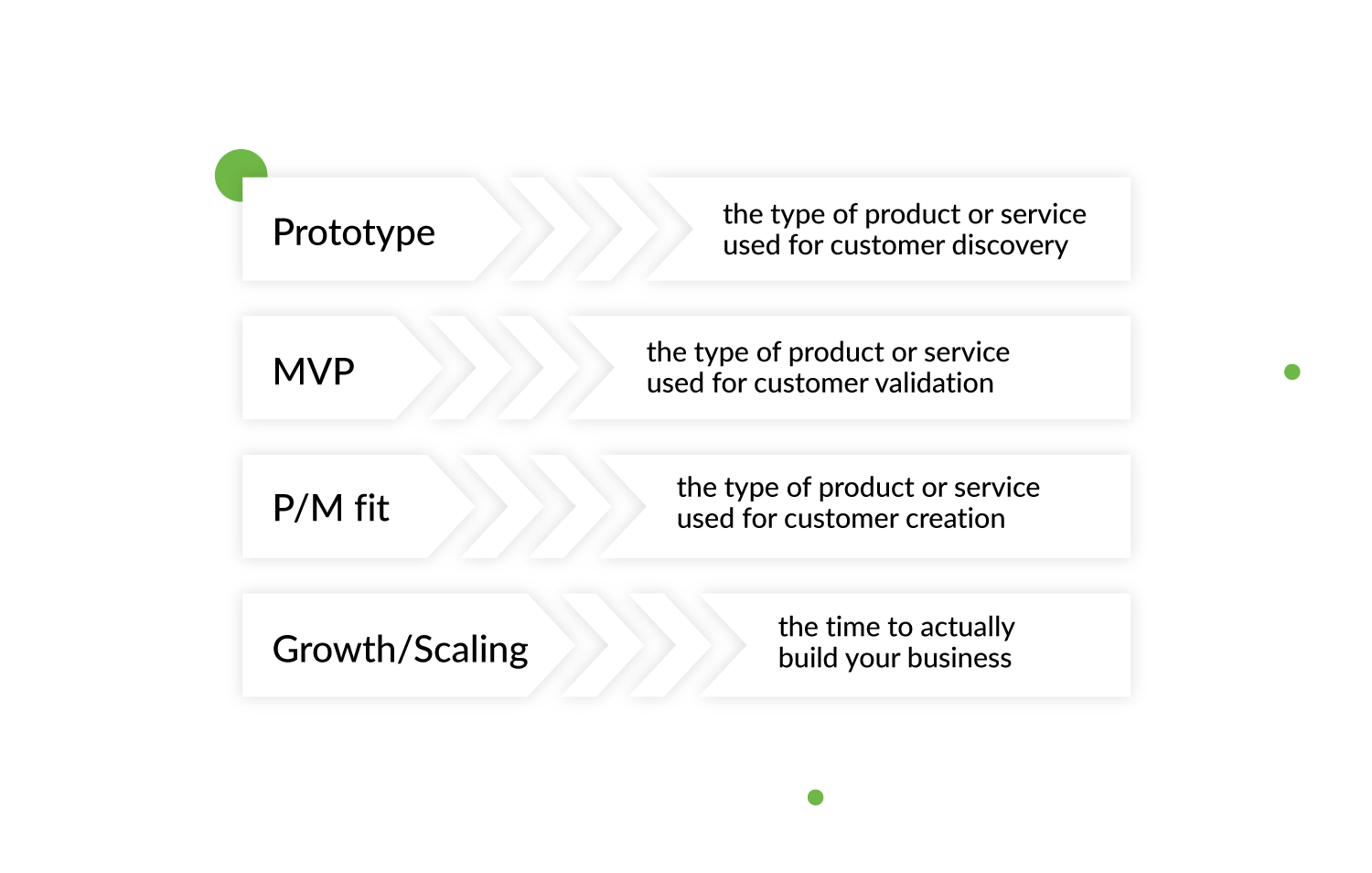

Before reaching the scaling phase, every new business has to go through 4 main stages: prototyping, MVP, product/market fit, and business growth.

Once you have a blueprint prototype of your idea, it’s time to test it on your audience. An MVP is a product that has the minimum set of features that allows you to find out what your customers want. MVP development services will help you to analyze the pain points of your audience and figure out how your product can solve them.

Here are our tips on how to build a fintech startup using MVP:

Don’t roll out a product stuffed with features that your audience might not need. First of all, you have to validate your idea and test your assumptions. The best way to do this is to create a version with a minimum set of features to learn more about your end-users’ needs. You can read more about MVP development in our Guide to MVP, MMP, MLP, MDP, and MAP startup stages.

Gathering initial feedback and analyzing it is the most important stage in the MVP development process. Your ability to analyze the results, observe the behavior of your users, and listen to their preferences will influence the success of your product roadmap.

The MVP is a journey, not a destination. You should continuously identify assumptions, find new ways to test them on your audience, analyze the results, and make changes to your product. The fact is, you will never intuitively know what works in your strategy. The best way to check it is to put your ideas in front of your audience as soon as possible.

Need more in-depth information about creating a fintech product that will be a hit in the market? Download our ebook to learn what you should consider when developing a financial solution.

Here we share our best practices, technical solutions, management tips, and every useful insight we’ve got while working on our projects

When thinking about how to start a fintech business, you should also keep in mind the overall industry focus on innovation. One advantage of fintech over traditional financial institutions is its ability to quickly change, provide additional services, adapt to the customer’s needs, and offer better solutions. Your startup ideas must be implemented in a few months to find their market fit and be able to compete with traditional financial institutions. Plus, fintech is full of additional services, so your system has to be flexible.

If you are looking for technical partners for a fintech startup, I assume you are not familiar with the technology required to actually build it. The point here is to trust the fintech development company when choosing the technology. The choice depends on multiple factors, one of them being the business goal you want to achieve with your product.

You should also know the restrictions associated with using a particular technology. One outcome of the right choice is a minimized risk that your entire project will be shut down if a new law comes out and you need to change something in the system to comply with new regulations or customer needs.

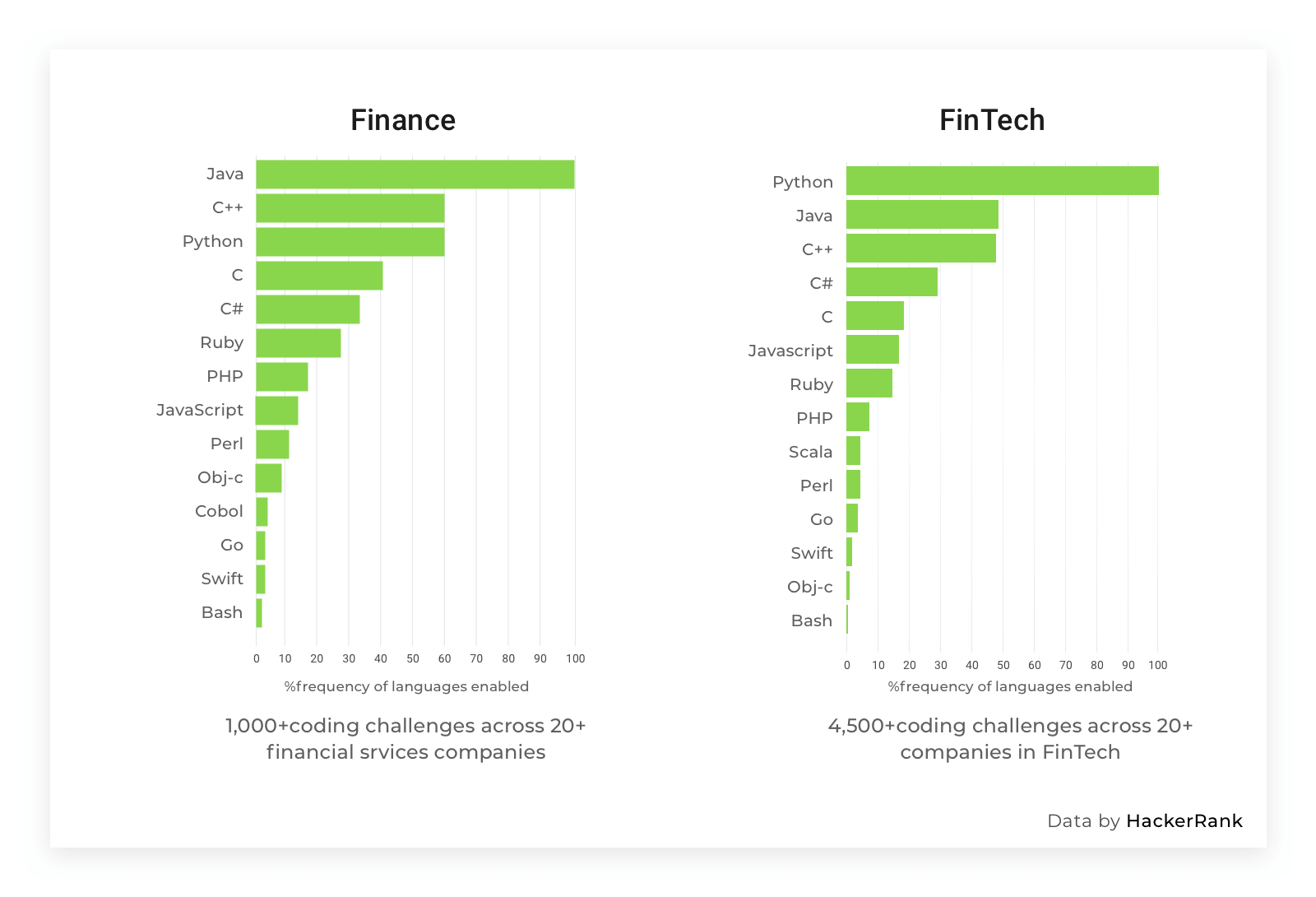

Some programming languages are rumored to be better and faster; others have proved to be best suited for particular types of projects. Many consider Python a great choice for fintech development, which is confirmed in HackerRank research. And with the Django framework, an MVP can be designed in a few months so that you can launch it ASAP. Python for fintech is flexible—it lets you adapt and change the finished product as much as you need.

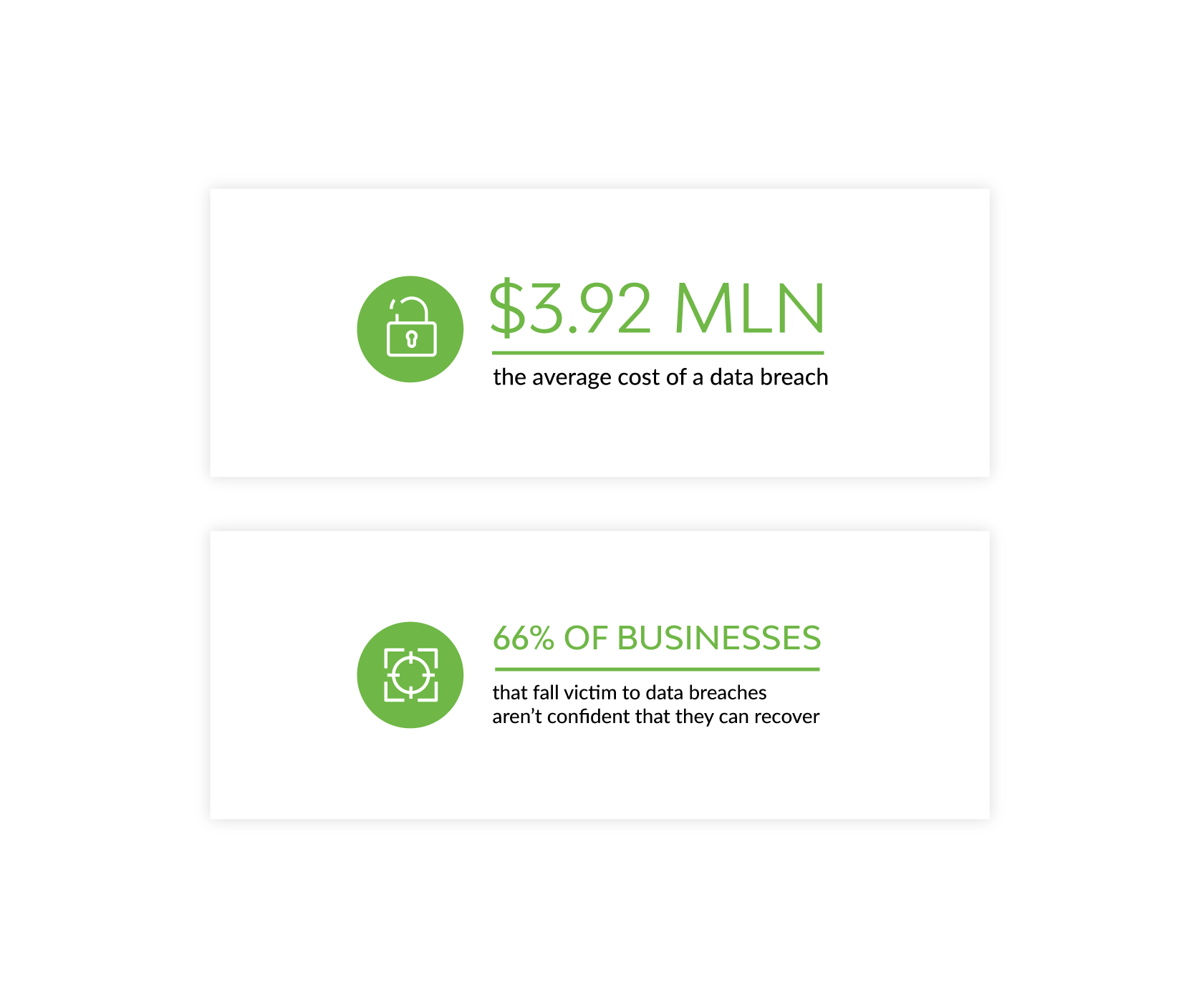

Data breach—this phrase is a nightmare for companies that work in fintech and a real threat to both their reputation and customer trust. Security is an essential feature you should invest your time and resources into. Its neglect may lead to severe circumstances and cost you a lot.

For example, UniCredit recently reported a breach of three million records among their Italian customers: their names, cities, and emails. Since 2016, UniCredit has invested €2.4 billion in upgrading its IT systems and cybersecurity. The bank immediately began investigating and informed its customers.

When we talk about data breaches, the statistics are really impressive. According to IBM, the average cost of a data breach amounts to $3.92 million, and 66% of businesses that fall victim to a data breach aren’t confident that they can recover from it.

All this information indicates that cybercriminals actively attack banks and other financial institutions. Neglect of security measures costs companies not only money—it also costs them customers.

How to start a fintech bank that can deal with this? I’ll give you some tips in the next section.

When it comes to fintech, security is your priority. The following tips will help you come up with a secure product.

Tunneling protocols are used within a virtual private network, which makes them effective at fintech data encryption. Here are some of the most popular protocols you can use for your fintech product:

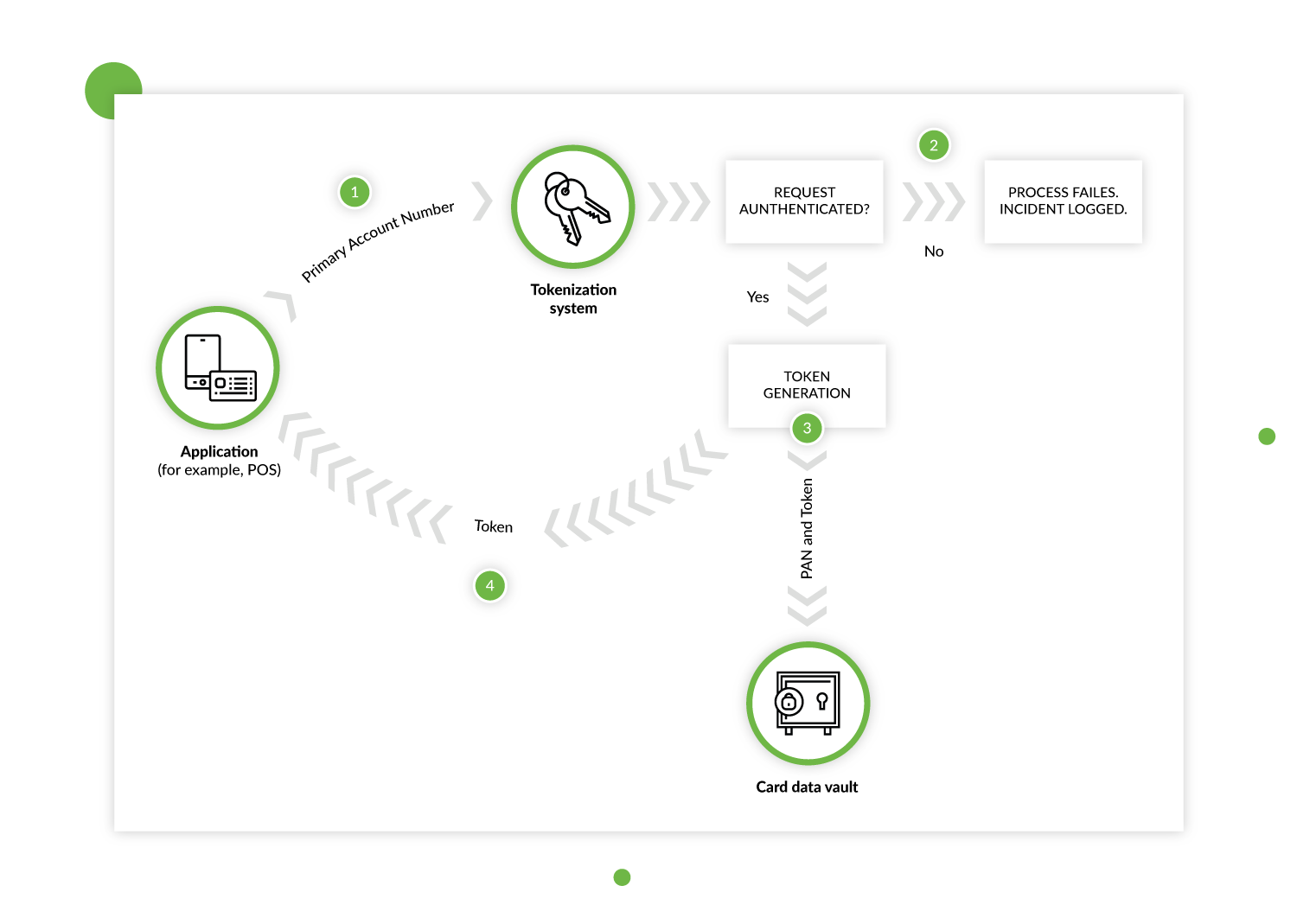

Tokenization is the process by which the primary account number (PAN) is replaced with a surrogate value called a token. Storing tokens instead of PANs can help to reduce the amount of cardholder data in the environment and limit the risk of a data breach. An example of the tokenization process is below:

Fraud detection systems analyze the client’s behavior and buying habits, and when something falls outside the usual patterns, unique security mechanisms are triggered.

AI is also very effective at preventing money laundering. For example, HSBC partners with the AI tech startup Ayasdi to identify fraud patterns, reduce the number of false alerts, and analyze linkages between accounts, customers, and related parties. There are a lot of other examples of AI in financial services that prove how this technology can take the industry to a new level.

Organizations embrace blockchain for protection; to go further, create your own blockchain with custom rules, auditability, and access models. One way to implement blockchain in your fintech product is to use decentralized storage solutions. They allow you to keep all your data in the blockchain and give access to third parties. In this way, hackers cannot access entire repositories of your data in one place.

Another use of blockchain technology is private messaging. Blockchain stores communication data across a decentralized network of nodes, removing centralized control of personal data and the possibility of personal data breaches.

One disadvantage of fintech is its dependence on traditional institutions. When you ask yourself how to build a fintech product, you need to take care of this as well. As the goal is to improve the user experience with financial products, you will need lots of integration with third-party services. What is integration in this case?

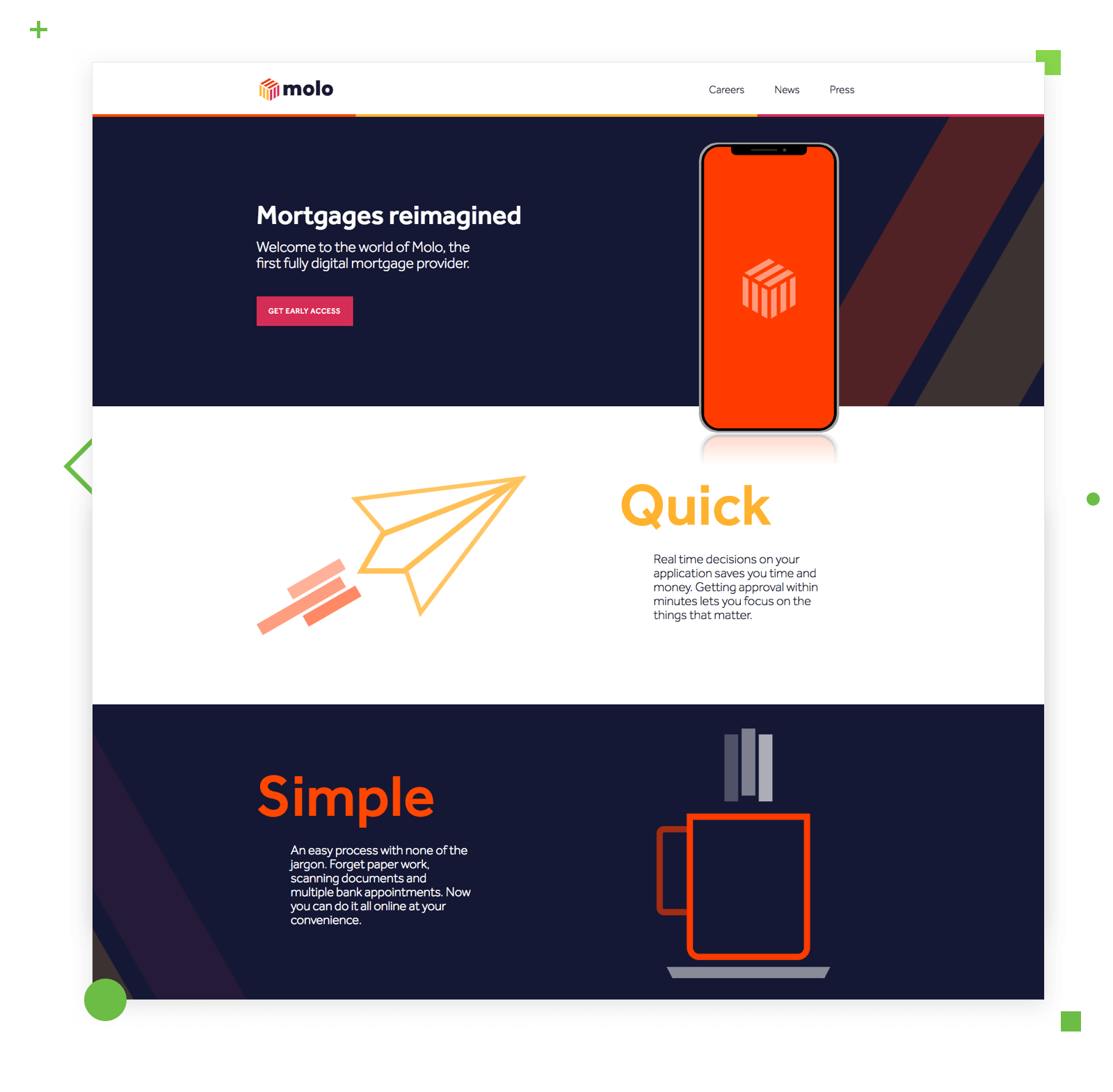

When using Molo (another online mortgage system we’ve been working on), users can choose houses they like and get a mortgage. When they want to get a mortgage, the system sends a request to organizations that can identify the users’ data (like Experian in the UK), and another request to verify the property. All these integrations make it possible to call Molo a fully digital mortgage provider and enable customers to go through the whole mortgage process online.

You need to predict as many needs as you can, for each will require time to implement. Remember that traditional financial services presuppose lots of bureaucracy, thus delays.

For instance, you will not reach the employees of a bank outside their working hours. Most likely, your users will not either. Your task here is to think how you can make the system work independently, or at least make it seem to.

At some point when developing MoneyPark, we had to integrate an insurance company API into the system. However, the insurance company would not allow direct communication between us, so we had to first communicate with MoneyPark. Only then would our message go to the insurers. We wasted hours because of this bureaucracy, and it is still the same in 2018. Traditional finance services are not very agile, but your users do not need to know it.

In the traditional finance system, there is always someone who gets a loan and someone who gives it. In insurance, there is an insurer and an insured. The same applies to fintech solutions. The technology should suit not only the end-customer, but the service provider as well. For that reason, most fintech startups are platforms that offer different functionality depending on the user role—just like Airbnb, which works one way for travelers, and another way for hosts.

For instance, a lot of fintech services provide access to their product to credit experts or financial advisors. That’s how they cover both B2B and B2C segments—working with end-customers as well as third parties. In this case, the fintech app development process includes the formation of different interfaces and features for each party because each performs actions peculiar to their role.

Basically, you need to consider the possibility of B2B interactions when choosing tech solutions and building a business model. Even if you’re not implementing it in your MVP, it might become a thing later.

This point continues the ideas I briefly mentioned in Part 2. Fintech stands between two major fields: finance and technology. To launch a fintech product that follows the state regulations, does not confuse users, and fits the market, you need to have a product owner with experience in both fields. Startups can come across the pitfalls of finance by neglecting certain terms or laws. However, the product owner should be responsible for the key element of the fintech product development process, which I have also mentioned previously.

Communication is one of the elements that defines whether the product will be a success or a failure. I am not saying that proper communication between you and your team will immediately ensure success. But it certainly reduces the chances of failure. The more you stay in touch with your team, the easier it is to prevent bugs and stick to the specified requirements of a product.

This is crucial if you and the engineers are in different time zones. Remember that most financial institutions work 9 to 6, so their APIs, tech support, and management are available during those hours as well.

DjangoStars is a renowned provider of fintech product development services for companies, projects, and startups of any scale and niche. DjangoStars has spent over fifteen years mastering its financial technology stack, collaborative flexibility, and approaches to industry standards and regulations. It is a proven security-first candidate (with ISO 27001 and ISO 9001 certifications in place) for finance-heavy projects. Django’s savvy fintech product programmers have delivered entire banking apps, payment integrations, and bank portals.

Itexus is a dedicated fintech product development company that focuses on solutions for banking and financial services. The company stands out for its fintech specialization, combining financial consultancy and complex software engineering. Itexus is also a niche expert in neobanking and digital payment solutions, delivering both white-label banking portals and full-on custom, AI-driven lending platforms.

Praxent is a financial product agency that consults, engineers, and modernizes fintech software, including lending platforms, banking systems, and AI payment integrations. Praxent boasts over twenty-five years of focused expertise in financial product development, providing ecosystem-ready, SOC II Type-I certified services. It also specializes in the modernization of existing banking and financial systems into evolutionary architectures that can be scaled easily in the long term.

TechAhead is an AI-first provider of fintech product developers and specialists in the latest intelligent software and platforms for finance. Boasting a portfolio of fintech products for some huge names (e.g., American Express), TechAhead offers bank-grade security and mobile-first innovation strategies, handling any finance-related needs. It is a great candidate to build a secure architecture with protected data and run it under the SOC 2 Type II and ISO 27001 certifications.

Idea Usher is a software agency with broad expertise, including digital marketing, blockchain, and integrated finance. It is a full-cycle technology partner that has built traditional payment integrations and in-depth blockchain applications. The agency handles everything from prototyping to launch and support of neobanks and payment engines. Idea Usher can be hired as a financial product firm, handling digital banking and marketing intricacies with proven experience and successful portfolio cases.

The tips I have described will not ensure the immediate success of your startup, but they are a good way to avoid the pitfalls of the industry in the early stages of creating a fintech app. To start with, find experts in building fintech teams who will help learn the nuances of the industry. That done, analyze the sector you are going to enter to better understand what sort of technical partner you will need.

As Don Norman, the author of the best-selling The Design of Everyday Things, once pointed out in his self-proclaimed Norman’s Law: “The day the product team is announced, it is behind schedule and over its budget. However, you can still make it in time if you choose the right technology and work with the right people to launch an MVP. But who is ever on time, anyway?”

Pay attention to the following recommendations:

Remember, ensuring the security of your fintech product is an ongoing process that requires constant vigilance and proactive measures.

Hire experienced developers to build your next project with DjangoStars